Over the past 30 years, high-yield and distressed debt have evolved into respectable and massive asset classes. What does the future hold for junk bonds? |

By Edward I. Altman

ne of the most remarkable developments in finance in the past few decades has been the way in which high-yield “junk” bonds and securities of distressed companies have gained legitimate status as important alternative asset classes for many types of institutional investors. Nearly 30 years ago, the high-yield bond market consisted almost entirely of “fallen angels” – bonds that were investment grade at birth but whose ratings were cut as the issuing companies’ fortunes sagged. And it was tiny. Less than $10 billion of such bonds were outstanding in the United States in 1978. Since then, the market has enjoyed spectacular growth, with more than $1 trillion in high-yield bonds outstanding in the US this year. And today, the market is dominated not by fallen angels but by newly issued non-investment grade securities. (Non-investment grade bonds are those that receive ratings from Standard & Poor’s and Fitch of below BBB-, or Moody’s ratings of below Baa3.)

Companies in emerging markets and in Europe now also routinely issue these securities. The relatively favorable risk-return attributes of high-yield bonds, and of its private-debt, leveraged-loan analog, regularly attract new annual investments of at least $100 billion each in the US and of increasing amounts abroad. In addition, the US has seen a substantial rise in the syndicated loan market. Syndicated lending has risen more than 60 percent in the last three years, and rose to $1.5 trillion in 2005. The growth in this sector has been paced by more risky leveraged loans. Leveraged loans, defined as loans of $100 million or more of companies with non-investment grade bonds outstanding, or whose loans yield about 125 basis points (1.25 percent) over an appropriate risk-free benchmark, are now estimated to be about $500 billion, or about one-third of the total syndicated loan market. Increasingly, these loans are being supplied by non-bank financial entities.

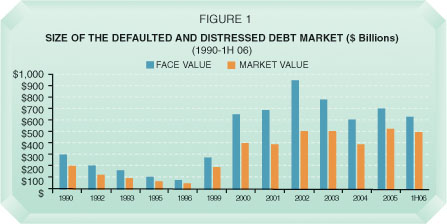

In another sign of growth and maturity of speculative grade fixed-income debt securities as an asset class, a new breed of distressed debt investors, called “vulture” funds, has emerged as one of the fastest growing sectors of the burgeoning hedge fund and private equity field. Distressed debt, a subgroup of the high-yield bond market, is defined as securities that yield at least 10 percent (1000 basis points) above the risk-free rate benchmark, and defaulted debt is defined as securities that trade after the issuing firm has missed an interest payment and/or has filed for bankruptcy. In the United States alone, we estimate that as of June 30, 2006, the size of the distressed debt market was about $620 billion in face value and about $500 billion in market value (see Figure 1). A similar amount, or more, is also attracting investors in Asia, particularly from Japanese and Chinese banks, and in Europe from German and Italian banks, among others.

The impressive growth in low-grade and distressed debt has spurred the development of statistics, analytics, and models that seek to explain and predict these markets’ size and risk-return trade-offs. Investors are constantly focusing on the outlook of these markets in order to develop strategies and to use market forecasts to attract new capital. Over the years, I have constructed numerous models and forecasts for the assessment of market dynamics of high-yield and distressed debt. Until very recently, these models have been quite accurate (annual reports can be seen at the website of NYU Stern’s Salomon Center, www.stern.nyu.edu/salomon). Forecasts of default and recovery rates on defaulted bonds that use mortality-actuarial methods and statistical regression techniques are now well-known and accepted by market participants and scholars.

But as is readily apparent from examining the history of high-yield bonds, markets are dynamic and constantly shifting. And there are times when even the most carefully constructed and tested forecasting models can be off the mark. The last few years have been one such period. Given the unique environment of the last several years, which has been fueled by massive liquidity and the advent of new participants like hedge funds, it is worth asking whether historically based estimates of default probabilities and recovery rates are still relevant for banks and hedge funds in today’s credit environment.

But as is readily apparent from examining the history of high-yield bonds, markets are dynamic and constantly shifting. And there are times when even the most carefully constructed and tested forecasting models can be off the mark. The last few years have been one such period. Given the unique environment of the last several years, which has been fueled by massive liquidity and the advent of new participants like hedge funds, it is worth asking whether historically based estimates of default probabilities and recovery rates are still relevant for banks and hedge funds in today’s credit environment.

Changing Forces

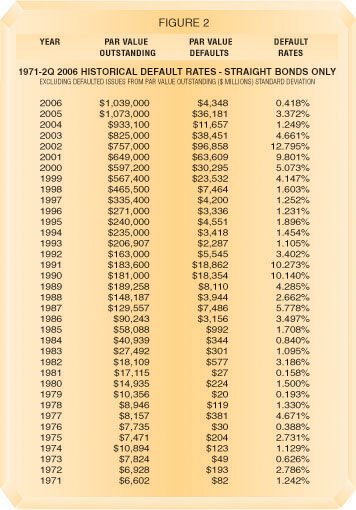

Traditional measures of defaults and default rates involve the comparison of the dollar amount of defaults from a particular market, such as the high-yield bond market, with the amount outstanding as of the beginning or the mid-point in a year. Figure 2 shows the default rate calculation from 1971 to the second quarter of 2006, and indicates that the weighted average default rate over the 36-year period is about 4.65 percent per year. The rate was a minuscule 0.42 percent for the first half of 2006. An alternative method, used by most rating agencies, involves the number of high-yield issuers rather than the dollar amount of defaults. And this rate is also very low of late.

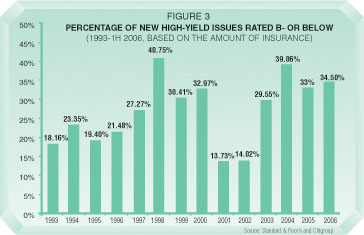

Historically, the default rate has experienced spikes in periods when the economy was entering a recession or a slowdown. The default rate since 2002 has been relatively low, especially in 2004 and 2005, with the exception of some rather large bankruptcies that contributed high amounts of defaults in the second-half of 2005, among them Delta and Northwest Airlines, auto parts maker Delphi, and the energy company Calpine. And in the first half of 2006, the default rate was extremely low by historical standards. Yet, using an actuarial-mortality rate approach that we developed in 1989 (which has been quite accurate in most years), we have consistently over-estimated default rates in recent years, with the exception of 2005. This technique analyzes the credit quality of new issues in the entire corporate bond market. We estimate future defaults based on the historical incidence of defaults to these new issue credit quality cohorts. In other words, by examining the quality of newly sold bonds at a given time, we have generally been able to project the rate of default for future periods. For example, Figure 3 shows that the proportion of newly issued “junk” bonds rated B- or below (the so-called bad cohort) has risen sharply starting in 2002, which would normally indicate increased defaults two to four years after issuance. But the expected increase in defaults to which the data points to simply has not manifested. Why?

Historically, the default rate has experienced spikes in periods when the economy was entering a recession or a slowdown. The default rate since 2002 has been relatively low, especially in 2004 and 2005, with the exception of some rather large bankruptcies that contributed high amounts of defaults in the second-half of 2005, among them Delta and Northwest Airlines, auto parts maker Delphi, and the energy company Calpine. And in the first half of 2006, the default rate was extremely low by historical standards. Yet, using an actuarial-mortality rate approach that we developed in 1989 (which has been quite accurate in most years), we have consistently over-estimated default rates in recent years, with the exception of 2005. This technique analyzes the credit quality of new issues in the entire corporate bond market. We estimate future defaults based on the historical incidence of defaults to these new issue credit quality cohorts. In other words, by examining the quality of newly sold bonds at a given time, we have generally been able to project the rate of default for future periods. For example, Figure 3 shows that the proportion of newly issued “junk” bonds rated B- or below (the so-called bad cohort) has risen sharply starting in 2002, which would normally indicate increased defaults two to four years after issuance. But the expected increase in defaults to which the data points to simply has not manifested. Why?

Increased Liquidity

To answer this question, it helps to look at trends in the investing landscape. The lower default rates have coincided with a rise in the number and size of hedge funds and private equity firms that employ related investment strategies. The driving force behind all of these strategies is the enormous increase in liquidity stimulated by the quest for higher yields and returns. The presence of so many investors with large amounts of money to deploy in the sector has, in the short run, along with a fairly robust economy and persistently low interest rates, lessened the incidence of defaults. (Both the robust economy and the persistently low interest rates have recently shown clear signs of change.) Indeed, the huge returns observed on low-quality assets in 2003, and the impressive but somewhat lower returns in 2004, fueled an already frothy distressed debt market in the aftermath of the enormous increase in defaults in 2001 and 2002.

In recent years, highly leveraged home owners have been less likely to default on their mortgages because the mortgage industry continually develops new products that allow them to restructure debt. A similar dynamic is taking place in the high-yield debt market, where companies in distress have a wider range of options – beyond default. Until recently, firms that got into trouble went to their traditional sources of financing – banks, insurance companies, and bond markets – to provide refinancing packages that could rescue them from temporary stressed conditions. But in the aftermath of the enormous default and loss experience of the early years of this decade, these traditional sources were reluctant to lend to newly distressed firms. Non-traditional sources, such as distressed debt hedge funds, saw an opportunity to fill the rescue financing void at attractive yields – e.g., double the spreads on comparably rated companies. These investors, flush with new capital infusions after they posted huge returns in 2003, have proven more willing to take subordinated positions than the traditional senior-secured lender. This has accounted for the impressive growth in the second-lien market of notes and bonds. Such loans bear interest of 500 to 600 basis points above LIBOR. And in order to hit the funds’ hurdle rates, leverage of two to three times is being used. Investors argue that private rescue financing packages (e.g., notes with warrants attached) can be structured to ensure relatively high recoveries if the rescue financing is not successful. Still, it is easy to observe that recent public and private financings have very weak or no protective covenants. Is the time bomb ticking away?

But investors aren’t just seeking to keep leveraged companies on life support; they are seeking to use high-yield debt as a means of getting involved with corporate governance or taking control of companies. “Active investing” has always been evident in distressed investing. There are numerous anecdotes of successful ventures, whereby the debt investor with large positions uses its position to influence the valuation of the reorganized company to receive a greater slice of the emerged-company pie. In some circumstances, including Sunbeam, Kmart, Barneys, and LTV/Bethlehem Steel, the active investor was also involved in a control situation – i.e., the investor winds up running the company when it emerges from bankruptcy.

But investors aren’t just seeking to keep leveraged companies on life support; they are seeking to use high-yield debt as a means of getting involved with corporate governance or taking control of companies. “Active investing” has always been evident in distressed investing. There are numerous anecdotes of successful ventures, whereby the debt investor with large positions uses its position to influence the valuation of the reorganized company to receive a greater slice of the emerged-company pie. In some circumstances, including Sunbeam, Kmart, Barneys, and LTV/Bethlehem Steel, the active investor was also involved in a control situation – i.e., the investor winds up running the company when it emerges from bankruptcy.

Or, active distressed debt hedge funds have provided rescue equity buyouts, further reducing the default rate. For example, Asprey & Garrard, the venerable English luxury jewelry retailer, was recently rescued by an American distressed hedge fund managed by Plainfield Asset Management, a firm run by NYU Stern Adjunct Professor Max Holmes. General Motors is in the process of selling a majority stake in its finance unit, GMAC, to Cerberus Capital, a huge hedge fund/private equity firm that specializes in distressed situations. The one-year probability of a GM default was considerably greater before the announcement of the proposed sale to Cerberus.

Success in these ventures has motivated more traditional private equity firms to enter the distressed firm space. And that has led to more purchases of distressed firms that investors believe can be viable, given new management and a new capital structure. This additional liquidity in the distressed firm market, both from traditional and non-traditional “vultures,” has no doubt reduced the number of defaults from the levels that might be expected.

New Paradigm?

The greater liquidity can be a double-edged sword. While it is certainly saving some firms from default, it could be laying the groundwork for more potential defaults down the road. Aggressive financing packages for struggling companies and merger activities are adding significant new leverage to corporate balance sheets. Debt-to-cash flow ratios have risen to above six in some of these transactions. Our research has shown that unless debt is reduced to manageable levels in two to four years after the highly leveraged transactions, we could experience firm meltdowns similar to what we saw in 1990 and 1991 – years in which the default rate rose to approximately 10 percent. This will be even more likely if the economy itself experiences a coincidental slowdown and interest rates rise. In the meantime, however, default rates remain relatively low.

A crucial metric for investors in this arena is the percentage of the face value of defaulted debt that will be paid back if there is a default – the recovery rate. Our research has clearly shown a significant negative correlation between coincident default and recovery rates. In other words, when default rates rise, recovery rates fall; and vice versa. Here, again, however, the dynamics seem to be changing. Forecasted recovery rates based on a supply/demand relationship for defaulted securities were quite accurate until 2005. But in 2005, our forecasted recovery rate (about 40-45 percent) was much lower than the actual rate (about 60 percent). This is another example in which the use of historical data has proved problematic in today’s unusual environment.

The key question today, therefore, is whether the benign credit environment, fueled by significant liquidity from traditional and non-traditional institutions, will continue to affect the high-yield, leverage-loan, and distressed debt markets. Or will the hot money recede, moving to other uses – commodities, alternative energy stocks, emerging markets, real estate – and the more normal default and recovery patterns return based on firm fundamentals. I believe that the latter scenario will manifest, perhaps toward the end of the second half of 2006 or, more likely, in 2007. And some of the hedge funds that used a good deal of leverage will find it difficult to cover their own loan requirements, as well as the inevitable fund withdrawals, given a fall-off in returns. But as investment managers like to say, the past is not necessarily a perfect guide to future performance. If the 2006 default rate remains at historically low levels, our 4 percent default rate forecast for 2006 will significantly over-estimate the reality, and the recovery rate will remain much above average. In other words, investors may continue to find valuables in the junkyard.

Edward I. Altman is Max L. Heine Professor of Finance at NYU Stern.

| On November 9, 2006, NYU Stern will host a Feschrift and gala dinner in honor of Professor Altman’s 65th birthday and 40 years of service to NYU Stern and the global financial community. A presentation of research and conference focused on credit risk, distressed debt investing, and restructuring will take place earlier in the day. For tickets to the gala or for more information, call 212-998-0383. |