![]()

|

|

decolonization dividend in the form of a 25 percent tax cut. But a case can be made that the British Empire was economically beneficial, not only to Britain herself, but also to her Empire and perhaps even to the entire world economy. In fact, when we consider its influence on capital and labor flows, on creating and promulgating the infrastructure that supports economic development, it is clear that the British Empire was a major force for global integration. Call it Anglobalization. It s now widely accepted that protectionism in less developed economies was one of the principle reasons for widening international inequality in the 1970s and 1980s. When they compared per capita (GDP) growth among developing countries, economists Jeffrey Sachs and A.M. Warner found that the open economies grew at 4.49 percent per year, and the closed countries grew at 0.69 percent per year. In the previous era of globalization the period from the mid-19th century until the First World War economic openness was imposed by Britain (and the other colonial powers) not only on Asian and African colonies, but also on South America and even Japan. A similar point can be made with respect to flows of labor. The more free movement there is of labor, the more international income levels will tend to converge. One reason that modern globalization is associated with high levels of inequality is that there are so many restrictions on the free movement of labor. But the British Empire actively promoted emigration. Consider also the evidence on international capital flows, another key component of globalization. According to the simple classical model of the world economy, capital should flow naturally from developed to less developed economies, where returns are likely to be higher. But as Robert Lucas, the Nobel Prize winning economist, has pointed out with respect to the United States and India in the 1970s, this does not seem to happen. Although some measures of international financial integration seem to suggest that the 1990s saw bigger cross-border capital flows than the 1890s, in reality most of today s overseas investment takes place within the developed world. In 1996 only 28 percent of foreign direct investment went to developing countries; by 2000 their share was less than a fifth. The overwhelming majority takes place between the United States, the European Union, and Japan. Investors in the developed world prefer to invest in countries with high levels of per capita GDP.

Did Empire Encourage Investment? In the first era of globalization the share of cross-border capital going to poorer countries was significantly larger then than it is today. In 1997 only around five percent of the world stock of capital was invested in countries with per capita incomes of 20 percent or less of U.S. per capita GDP. In 1913 the figure was 25 percent. In 1995 the share of developing countries in total international liabilities was 11 percent, compared with 33 percent in 1900 and 47 percent in 1938. Those figures suggest the possibility that the existence of formal empire encouraged investors to put their money in less developed economies. Finally, we need to consider recent empirical work on the institutional and political preconditions for growth. The historian David Landes has argued that the ideal growth-and-development government would secure rights of private property (the better to encourage saving and investment) and enforce rights of contract. Such a government would be stable, honest, responsive, governed by publicly known rules, and hold taxes down.

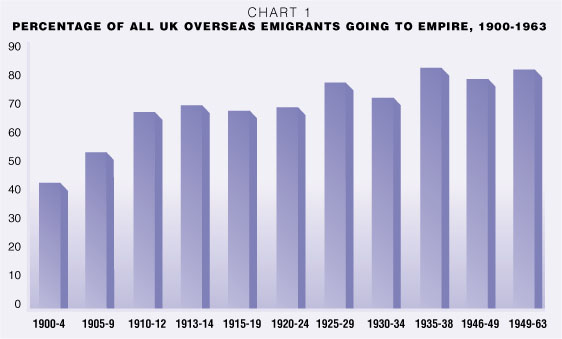

According to one estimate, the economic benefit to Britain of enforcing free trade could have been anywhere between 1.8 and 6.5 percent of GNP. But what about the benefit to the rest of the world? As one eminent Victorian put it, Britain was the great Emporium of the commerce of the World. Between 1871-5 and 1925-9, the colonies share of Britain s imports rose from a quarter to a third. More generally, as Jeffrey Williamson has argued, it was (mainly British) colonial authorities that resisted protectionist backlashes to the dramatic falls in factor prices caused by late 19th-century globalization. In the same way, there would not have been so much international mobility of labor and hence so much global convergence of incomes before 1914 without the British Empire. True, the independent United States was always the most attractive destination for 19th-century emigrants. But as American restrictions on immigration increased, the significance of the white Dominions as a destination for British emigrants grew markedly (see Chart 1). They attracted around 59 percent of all British emigrants between 1900 and 1914, 75 percent between 1915 and 1949, and 82 percent between 1949 and 1963. Nor should we lose sight of the vast numbers of Asians who left India and China to work as indentured laborers, many of them on British plantations and mines, in the course of the 19th century. Perhaps as many as 1.6 million Indians emigrated under this system. There is no question that the majority of them suffered great hardship. But we cannot pretend that this mobilization of cheap and probably underemployed Asians to grow rubber or dig gold had no economic significance.

Capital Exports From the mid-19th until the mid-20th centuries, Britain acted as the world s banker, channeling colossal sums of British (and other European) savings overseas. By 1914 total British assets overseas amounted to somewhere between £3.1 and £4.5 billion, compared with a British GDP of £2.5 billion. True, around 45 percent of British investment went to the United States and the Dominions. But 16 percent of British foreign investment went to Asia and 13 percent to Africa, compared with just six percent to the rest of Europe. As late as 1938, around 18 percent of British overseas assets were in Asia, and 11 percent in Africa. British investment in developing economies principally took the form of portfolio investment in infrastructure, especially railways. But the British also sank considerable sums directly into plantations to produce new cash crops like tea, cotton, indigo, and rubber.

Why were British investors willing to risk such an exceptionally high proportion of their savings by purchasing securities or other assets overseas? One possible answer is that the adoption of the gold standard by developing economies offered investors a Good Housekeeping seal of approval. Yet there is a need to distinguish here between anticipated and actual returns on overseas investments. For the period 1850 to 1914, anticipated returns were not significantly lower on colonial bonds than they were on other foreign bonds. But the same cannot be said of the actual returns. In a sample of 11 major capital-importing economies, if one takes an average of the three colonial countries Australia, Canada, and Egypt the anticipated yield was 5.3 percent, compared with 4.7 percent for the three South American countries in the group. But the actual returns were significantly different: 4.7 percent as against 2.9 percent. So when the same countries returned to the bond market in the inter-war years, they paid significantly different risk premia. On average, the returns Latin American borrowers had to offer investors were 270 basis points higher than those on new colonial issues. Even so, actual returns on Latin American bonds were once again worse than expected and worse than those on colonial bonds.

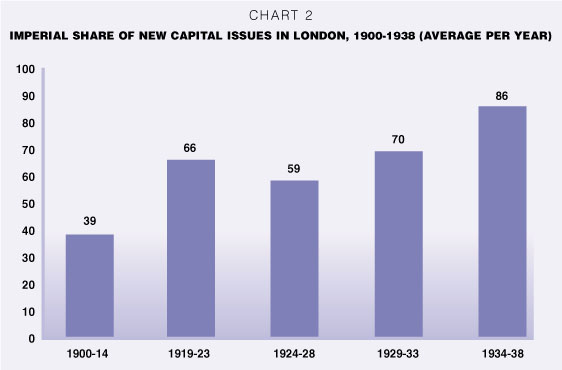

This sentiment explains why an increasing share of British overseas investment ended up going to the Empire after the First World War (see Chart 2). Between 1856 and 1914, approximately two-fifths of British overseas capital went to the Empire. But between 1919 and 1938, the Empire received two-thirds of such investment while the rest of the world got one third. Nor is it surprising that more than three-quarters of all foreign capital invested in sub-Saharan Africa was invested in British colonies.

Encouraging Imports For much of the 19th and 20th centuries, British economic policy was heavily influenced by the financiers of the City of London, with their ethos of gentlemanly capitalism. International finance came first and British export industries a poor second. In order to ensure that loans to developing economies were repaid, British policy-makers were prepared to go to considerable lengths, ultimately allowing a system of differential tariffs to evolve that gave colonial manufacturers easier access to the British home market than British manufacturers enjoyed to colonial markets.

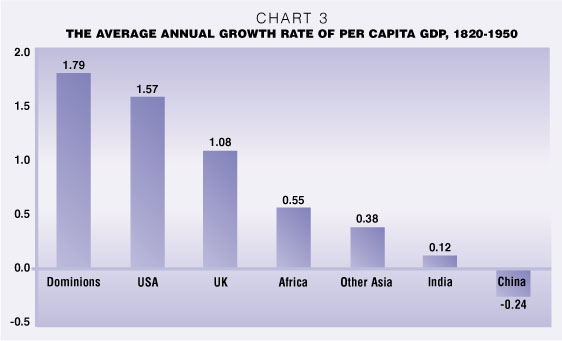

The British did not see the economic development of Asia and Africa as their primary concern. Nevertheless, the intended policy of financial rather than industrial domination of the world economy had secondary positive outcomes. Under the right circumstances, this policy was conducive to rapid economic growth on the periphery. The results of Anglobalization were in many ways astounding. The combination of free trade, mass migration and unprecedented overseas investment propelled large parts of the Empire to the forefront of world economic development. Canada, Australia, and New Zealand produced more manufactured goods per capita than Germany in 1913. Between 1820 and 1950, their economies were the fastest growing in the world. Indeed, per capita GDP grew more rapidly in Canada than in the United States between 1820 and 1913 (see Chart 3).

The Asian Exception But the performance of the Dominions was not matched in the rest of the Empire, least of all in Asia. India attracted £286 million of capital raised in London between 1865 and 1914 18 percent of the total placed in the Empire, second only to Canada. But between 1857 and 1947, Indian per capita GDP grew by just 19 percent, compared with an increase in Britain of 134 percent. Chart 3 shows that between 1820 and 1950, it grew at a mere 0.12 percent per annum.

Yet recent research casts doubt on key aspects of the nationalist critique. Economic historian Tirthankar Roy has shown that the destruction of jobs in the Indian textile industry was probably inevitable, regardless of who ruled India, and that an equal if not greater number of new jobs were created in new economic sectors built up by the British. Even in the case of textiles, by the 1920s the Government of India was clearly giving preference to Indian manufacturers over Lancashire s mills. Roy also casts doubt on the idea that taxation under the British was excessive. And the supposed drain of capital from India to Britain turns out to have been comparatively modest: only about 0.9 to 1.3 percent of Indian national income from 1868 to the 1930s, according to one recent estimate of the export surplus.

The explanation for the disappointing impact of these improvements in per capita incomes lies not in British exploitation, but rather in the insufficient scale of British interference in the Indian economy. The British expanded Indian education but not enough to make a real impact on the quality of human capital. The British invested in India but not enough to pull most Indian farmers up off the base line of subsistence. The British built hospitals and banks but not enough to make significant improvements in public health and credit networks. These were sins of omission more than commission. Unfortunately for Indians, the nationalists who came to power in 1947 drew almost completely the wrong conclusions about what had gone wrong under British rule, embarking instead on a program of sub-Soviet state-led autarky whose achievement was to widen still further the gap between Indian and British incomes, which reached its widest historic extent in 1973.

Economic historians continue to debate the causes of the great divergence of economic fortunes which has characterized the last half millennium. In this debate, the role of colonialism and specifically the British Empire has a crucial role to play. If geography, climate, and disease provide a sufficient explanation for the widening of global inequalities, then the policies and institutions exported by British imperialism were of marginal importance. However, if the key to economic success lies in the adoption of legal, financial, and political institutions favorable to technical innovation and capital accumulation, then it matters a great deal that between around 1880 and 1940 a quarter of the world was under British rule. In all likelihood, the dichotomy between geography and institutions is a false one. The British settled in large numbers in temperate zones, taking their institutions with them; in the tropics, they preferred to rely on monopoly companies and plantations run in (unequal) partnership with indigenous elites. But by the last third of the 19th century this distinction had faded somewhat. Even in the tropics, the British endeavored to introduce the institutions that they regarded as essential to prosperity: free trade, free (and indeed forced) migration, infrastructural investment, balanced budgets, sound money, and the rule of law and incorrupt administration. If the results were much less impressive in Africa and India than they were in the colonies of British settlement, that was because even the best institutions work less well in landlocked, excessively hot, or disease-ridden places. There, the investments which would have been needed to overcome geography, climate, and its attendant deleterious effects on human capital were beyond the imaginings of colonial rulers. Yet it is far from clear that the very different policies adopted by post-independence governments and international agencies have been more successful. A simple calculation of the ratio of British per capita GDP to that of 41 former colonies is instructive. Between 1960 and 1990 the gap between the British and their former subjects narrowed in just 14 cases. While it is convenient for contemporary rulers in countries like Zimbabwe to blame their problems on the legacy of British rule, the reality is that British rule was on balance conducive to economic growth. Tragically, most post-independence governments have failed to improve on it. Niall Ferguson is Herzog professor of financial history at NYU Stern and visiting professor of history at Oxford University. His most recent book is Empire: The Rise and Demise of the British World Order and its Lessons for Global Power (Basic Books), from which this article is adapted. © Niall Ferguson 2003.

|

||||||||||||||||||||||||||||||||