![]()

|

Several factors have contributed to this growth. The rise of fractional aircraft ownership has dramatically reduced the up-front costs of access to corporate jets. And in the wake of the September 11, 2001 terrorist attacks, many executives have chosen to escape the hassles and perceived danger of flying on major airlines by using private jets. Corporate jets regularly inspire criticisms of managerial excess by journalists and shareholder activists, and they frequently seem to symbolize corporate cultures of excess. At Adelphia Communications, the bankrupt cable company whose top executives have been convicted of fraud, prosecutors charged that the company jet was used to ferry corporate founder John Rigas to Kenya on a safari and to deliver a Christmas tree to one of Rigas’ daughters. At Enron, according to Bethany McLean and Peter Elkind, authors of The Smartest Guys in the Room, members of CEO Kenneth Lay’s family were known to use the company’s jet fleet as a sort of personal taxi service. But Adelphia and Enron provide only anecdotal connections between the use of jets and potential damage to shareholders. I set out to determine if there was, in fact, an empirical link between CEOs’ use of corporate jets and corporate performance. The results were striking. In the short-term, shareholders react negatively to the news that CEOs are using corporate jets. While CEOs who fly on such aircraft may arrive at their destination quickly, their stocks lag. The shares of companies whose CEOs use private aircraft under-perform the market by more than 400 basis points per year.

Perks and Compensation In a sense, this effort was a matter of putting two theories of executive behavior and compensation to the test. In their classic 1976 study, Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure, Michael C. Jensen and William Meckling, of the University of Rochester, used perquisite consumption by managers as the basis for their formal model of the agency costs of outside equity in a public corporation. When an owner-manager sells stock to the public and reduces his ownership below 100 percent, incentives increase for the manager to expend corporate resources for personal benefit. Jensen and Meckling’s model seems to predict that perk consumption by a CEO should vary inversely with his fractional ownership of the company (that it would rise as a CEO’s stake in the publicly-held company he runs falls). They also suggest a manager’s personal tastes and the difficulty of monitoring the manager’s actions would influence perk consumption.

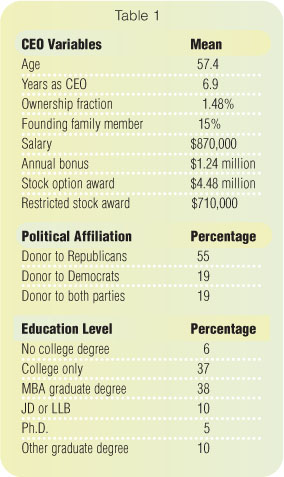

In his 1980 paper, Agency Problems and the Theory of the Firm, University of Chicago Finance Professor Eugene Fama took a more benign view of perquisites. “Consumption on the job” by managers amounts to a form of compensation that can be offset through adjustments in salary or other forms of pay. Fama described the interaction between managers and their boards of directors in terms of a dynamic of “ex post settling up,” in which the manager’s wage is regularly revised to account for his performance and his personal consumption of company resources. Fama’s model implies that perk consumption represents an agency cost only to the extent that its value exceeds the subsequent consequences to the manager from ex-post settling up wage revisions. Fama’s theory, then, appears to predict an inverse association between perk consumption and compensation, controlling for other attributes that affect compensation such as industry, performance, and experience. In other words, perk consumption would fall as compensation rises. Table 1 contains data on the characteristics of the CEOs in the study. The typical CEO was about 58 years old, with a mean ownership of about 1.5 percent of the firm’s shares. CEOs received mean cash salary and bonus compensation of about $2.1 million, and additional annual income from stock option and restricted stock awards. Stock options delivered a large, skewed distribution of compensation, with a mean of $4.5 million and a median of $1.6 million.

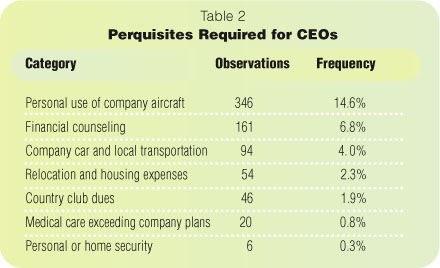

Measuring Perk Consumption Next, I measured CEO perk consumption – a complex and occasionally difficult task. The primary source of information was the companies’ annual proxy statements. Data on perks usually appear in proxies as a footnote to column (a) of the Summary Compensation Table, headed “Other Annual Compensation.” The total value of perks must be disclosed based upon their “aggregate incremental cost” to the company, but only if the total exceeds the lesser of $50,000 or 10 percent of the executive’s salary plus bonus. Companies must itemize the cost of any individual perk, such as personal aircraft use, if it exceeds 25 percent of the overall perk total, assuming that the total exceeds the $50,000 threshold. The structure of the Securities and Exchange Commission’s disclosure rules causes data for CEOs’ personal aircraft use to be censored. For example, assuming the CEO earns at least $500,000 salary plus bonus, firms never have to disclose aircraft use if its cost lies below $12,500 (equal to 25 percent of the $50,000 overall threshold). From reading a large number of proxy statements, it is evident that several disclosure loopholes limit the transparency of perk consumption data. What determines whether a CEO has a higher propensity to use corporate aircraft? I used a Tobit regression model to analyze how the cost of CEO aircraft use in each firm-year is related to a range of explanatory variables. Among the variables I chose were CEO stock ownership, compensation, the age of the CEO, whether or not he was a member of the firm’s founding family, education level, and political affiliation. The regression model includes control variables for size and capital structure.

The Jensen-Meckling theory of perks predicts that CEOs trade off the value of perk consumption against the reduction in personal ownership value entailed by that same consumption. When I estimated the model, the CEO ownership variable provided evidence of the predicted negative association with perk consumption. The estimates imply that increases in ownership act as a curb against perk consumption at both low and high ownership levels, but that greater ownership provides protective cover that CEOs use to extract greater perks over a middle ownership range. The overwhelming majority of CEOs in this sample lay in the low ownership range. Again, the effect was very small. The marginal effect implies that a 1 percent rise in CEO ownership leads to a $5,030 reduction in perk consumption, which seems quite small compared to the cost of the additional equity investment – $201 million in the mean sample firm.

Older Frequent Fliers

CEOs from founding families also use corporate aircraft with abnormally high frequency, perhaps indicating that founders do not recognize boundaries between personal and corporate property as clearly as non-founders. Political affiliation has some impact upon perk consumption, but in a non-partisan way. CEOs who make no political donations are the heaviest users of corporate jets, while CEOs who make donations to both parties are the lightest users. CEOs who clearly are Democrats or Republicans fall somewhere in the middle. Finally, the education variable results were striking. CEOs with the least education (no college degree) are the heaviest aircraft users, while those with the highest advanced degrees (Ph.D.s) are the lightest. CEOs who hold MBAs or other masters degrees are somewhere in between, and CEO-lawyers have significantly higher aircraft use than normal, though not as high as non-college graduates.

Shareholder Returns

How does aircraft use affect stock prices? In my 1993-2002 sample of 237 firms, 63 companies disclosed no CEO aircraft use for either of the first two years and then began disclosing it for some future year or years. I calculated the mean cumulative abnormal stock returns (CAR) for these 63 firms beginning two weeks – or 10 trading days – prior to the statement date of the proxy in which corporate aircraft use was first disclosed. I extended the event window until one day after the filing day because some firms may post their documents after the market closes. The results: stock prices exhibit essentially zero change until one week before the event day, at which point they begin to trend downward, with the mean showing a CAR of -1.99 percent. The CAR results indicate that shareholders do not welcome the news that firms permit CEOs to use corporate aircraft for personal travel. When I ran regressions that took into account compensation and ownership levels, I found that shareholder reactions to CEOs’ corporate jet use are mitigated if the CEO earns lower compensation. This pattern is consistent with Fama’s perspective, that perks are benign if offset by reductions in other forms of compensation.

Long Term Losses Short-term, stockholders plainly view the use of a corporate jet as a negative. Next, I assessed the ongoing market performance of firms that permit their CEOs to have personal use of corporate aircraft. Again, the results were negative. The results indicate that firms with CEO aircraft use under-perform the market by more than 400 basis points per year, equal to a shortfall of about $300 million in market capitalization each year for the median sample firm. Given that these performance shortfalls equal hundreds of millions of dollars per company per year, it would be difficult to argue that the direct costs of perk consumption alone could explain the gap. Even the most expensive jets don’t cost several hundred million dollars. One clear possibility is that these managers who use jets frequently also run their firms inefficiently, tolerating waste, excess overhead, or uncompetitive cost structures. When I ran regressions of firms’ return on assets against the aircraft use dummy variable, as well as dummy variables for industries and years, I found a negative association between profitability and the aircraft use variable, and a strong, significant negative association between the aircraft variable and sales per employee. These regressions indicate that firms with high CEO perk consumption also tend to be over-staffed relative to the competition, as they achieve $30,000 to $40,000 less in sales per employee. The inverse relationship between CEO aircraft use and company performance appears surprisingly strong and much larger than could be explained by the direct cost of the resources consumed. It could be that CEOs who consume excessive perks may be less likely to work hard, less protective of the company’s assets, or more likely to tolerate bloated or inefficient cost structures. High executive perks might also occur due to weak corporate governance. For many in the world of business, the corporate jet is the ultimate sign of arrival. When they’re able to fly in a Gulfstream IV out of Teterboro Airport in New Jersey instead of having to wait in line to board a Boeing 737 at La Guardia, many executives feel as if they have finally made it. For shareholders, ironically, this moment frequently signals it’s time to head for the exits. David Yermack is associate professor of finance at NYU Stern.

|

I tested both theories by investigating the

prevalence of a major perk – the use of corporate jets – and

then measuring its relationship to other factors such as overall

compensation, CEO characteristics, and shareholder return. Data

for this study was drawn from a panel of 237 Fortune 500 companies

between 1993 and 2002. The final sample had 2,340 observations,

with most firms appearing in the sample for 10 full years. Those

observations covered 485 individual CEOs, a small handful of whom

served more than one term with the same company. The sample firms

had median annual sales of close to $7 billion, median total assets

above $10 billion, and a median market capitalization close to

$8 billion.

I tested both theories by investigating the

prevalence of a major perk – the use of corporate jets – and

then measuring its relationship to other factors such as overall

compensation, CEO characteristics, and shareholder return. Data

for this study was drawn from a panel of 237 Fortune 500 companies

between 1993 and 2002. The final sample had 2,340 observations,

with most firms appearing in the sample for 10 full years. Those

observations covered 485 individual CEOs, a small handful of whom

served more than one term with the same company. The sample firms

had median annual sales of close to $7 billion, median total assets

above $10 billion, and a median market capitalization close to

$8 billion. The median cost to the company of CEO’s personal aircraft use,

when disclosed, is a little more than $50,000. While costs of operating

different aircraft vary greatly, The New York Times, using data from

Executive Jet Inc., the leading time-share company, in 2001 estimated

the hourly cost of leasing an eight-person Cessna Citation V aircraft

was $10,000 – or $2,500 per person if the CEO on average travels

with three other passengers. A CEO with $50,000 in reportable aircraft

use would therefore spend about 20 hours per year in the sky, enough

for perhaps three round-trips between New York and Florida, for example.

The median cost to the company of CEO’s personal aircraft use,

when disclosed, is a little more than $50,000. While costs of operating

different aircraft vary greatly, The New York Times, using data from

Executive Jet Inc., the leading time-share company, in 2001 estimated

the hourly cost of leasing an eight-person Cessna Citation V aircraft

was $10,000 – or $2,500 per person if the CEO on average travels

with three other passengers. A CEO with $50,000 in reportable aircraft

use would therefore spend about 20 hours per year in the sky, enough

for perhaps three round-trips between New York and Florida, for example. Variables associated with CEO tastes and preferences have clear impacts

upon patterns of corporate aircraft use. Older CEOs are more likely

than younger ones to make personal use of company aircraft. This

pattern may arise due to increasing frailty of CEOs as they age,

or it may represent opportunism by CEOs who consume perks heavily

near the end of their careers with reduced fears that ex post settling

up wage revisions will permanently impact their compensation.

Variables associated with CEO tastes and preferences have clear impacts

upon patterns of corporate aircraft use. Older CEOs are more likely

than younger ones to make personal use of company aircraft. This

pattern may arise due to increasing frailty of CEOs as they age,

or it may represent opportunism by CEOs who consume perks heavily

near the end of their careers with reduced fears that ex post settling

up wage revisions will permanently impact their compensation.