![]()

|

However, this approach comes with significant costs. To implement such systems appropriately, organizations must be able (and willing) to devote substantial resources to surveillance methods, so that employees feel that their rule-following or breaking behavior will be detected. Indeed, the extensive use of such surveillance techniques – cameras, the monitoring of telephone calls and computer usage, drug testing, time clocks, and ordinary managerial monitoring of employees – is testament to just how prevalent such systems are in the modern workplace. In addition to tangible costs, such systems have intangible social costs. The command-and-control approach typically communicates a message to employees that they are not trusted and that the organization is their adversary (and vice versa), leading to the breakdown of trust between employees and their organizations. Evidence also suggests that the success of this approach is limited. Employees intent on breaking rules often find ways to do so undetected. This often leads organizations to devote even more resources to surveillance, further adding to the tangible and intangible costs of those mechanisms. And even then, employees often find new ways to circumvent detection. The downward spiral of this approach can be debilitating to an organization.

What might breed an intrinsic desire among employees to adhere to organizational policies? In our work, we have focused on the influence of two judgments employees make about their work organizations. The first is the assessment by employees that there is congruence between their own moral values and those of the organization. That is, we predict that employees will be intrinsically motivated to follow their organization’s rules if they feel that those rules develop from a system that is consistent with their own set of moral values. The second judgment is the assessment by employees regarding the legitimacy of those with power in their organizations – i.e., whether employees believe that those who wield control over the rules of the organization are entitled to such control. We predict that employees will also be intrinsically motivated to follow the organization’s rules if they feel that those rules are developed and enforced by authorities they regard as legitimate. In sum, our research on the self-regulatory approach is based on the prediction that these two judgments foster an intrinsic desire on the part of employees to follow organizational rules, and, furthermore, that the intrinsic desire they inspire outweighs the influence of command-and-control mechanisms. We set out to test this prediction by creating studies that compare the relative efficacy of these two approaches for promoting three forms of employee rule-following: compliance, deference, and rule-breaking. Compliance refers to employee’s straightforward following of their organization’s rules. Deference refers to rule-following that is specifically discretionary in nature – i.e., do employees follow rules even when no one, including their bosses, will know that they did so? On the other hand, we also set out to consider the flip side of compliance and deference, which is rule-breaking. Rule-breaking refers to conscious decisions by employees to ignore or violate organizational rules or policies.

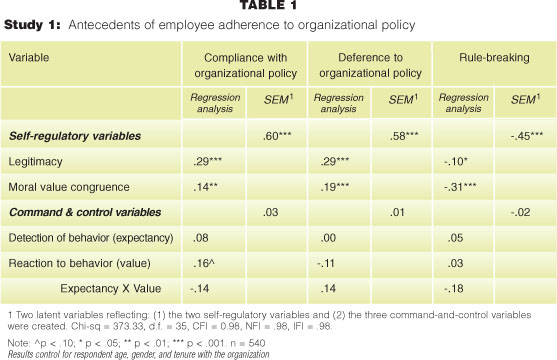

Testing Predictions The first study we conducted was based on confidential questionnaires distributed to the employees at a division of a multinational banking firm. The respondents held positions ranging from clerical to managerial, with the bulk of the employees involved in directly providing banking services to high-profile customers. A total of 540 surveys were returned. For those responding to the survey, the mean tenure with the firm was 13 years, the mean age was 42 years, and there was an average salary of $84,000. These characteristics mirrored those of the broader set of employees working in this division. Respondents were asked to respond to a series of questions about their rule-following. Sample questions, with responses on a scale of (1) never to (6) very often, included: “How often do you follow the policies established by your supervisor?” (for compliance); “How often do you follow organizational policies even when you do not need to do so because no one will know whether you did or not?” (for deference); and “How frequently do you neglect to follow work rules or the instructions of your supervisor?” (for rule-breaking). To assess the two judgments related to the self-regulatory approach, respondents indicated their agreement with statements such as “Disobeying one’s supervisor is seldom justified” (for legitimacy) and “I find that my values and the values of my company are very similar” (for moral value congruence). Finally, we asked two types of questions to assess the perceived incentives and sanctions for rule-following and behavior (i.e., to assess the command-and-control approach). First, to measure the expectancy that rule-following would be detected in the first place, we asked respondents questions such as “How much attention does your supervisor pay to whether or not you follow work rules?” Second, to measure the value employees placed on the incentives or sanctions for rule-following or breaking, we asked them questions such as “If you were caught breaking a work rule, how much would it hurt you?” Since it is possible that these types of judgments (i.e., judgments regarding expectancy and value) interact with one another, such that punishments or rewards only matter if they seem likely, we also included an interaction term in all our analyses to capture any such effects.

We also utilized an additional statistical analysis called structural equation modeling (SEM) to further investigate the relative influence of the self-regulatory and command-and-control approaches. Rather than examining the variables included under each approach individually, this analysis allows direct examination and comparison of the variables comprising each approach as a set. The results of these analyses, also presented in Table 1, confirm that the self-regulatory approach is a more effective way of fostering employee rule-following.

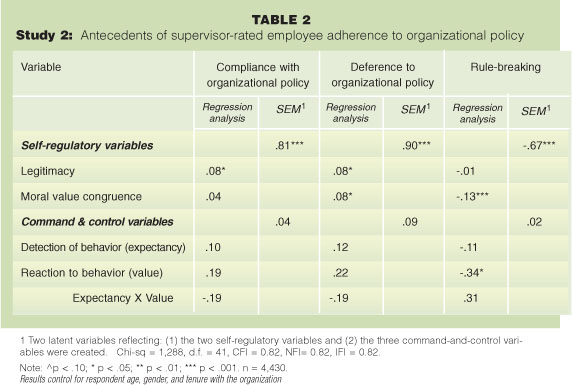

Additional Evidence The first study did not contain independent ratings of rule-following behavior, and thus raises issues related to self-report of behavior. For instance, perhaps respondents were not accurately reporting their own behavior. We conducted a second study to address this limitation. This study was based on a large sample of employees from around the United States, who worked in a wide variety of companies and industries. Importantly, we obtained supervisor ratings of employee rule-following for a significant subset of respondents to address this potential criticism of the first study.

First, we examined respondents’ self-report of their behavior, to determine whether the effects we found in Study One were replicated in Study Two. As in the first study, variables representing the self-regulatory (legitimacy and moral value congruence) and command-and-control (detection of behavior, reaction to behavior, and their interaction) strategies were regressed on each of the three types of rule-following. By and large, the results confirmed the findings from the first study. Specifically, legitimacy and moral value congruence were related to all three forms of rule-following, with evidence suggesting that legitimacy had a somewhat stronger effect than value congruence. However, in Study Two the command-and-control variables had effects not found in Study One. In particular, the belief that one’s work behavior would be detected (expectancy) was significantly related to all three forms of rule-following, and expectations about the reactions to detected behavior (value) also had a significant, though small, effect on compliance and rule-breaking. Structural equation modeling was again used as an additional way of exploring the relative impact of the self-regulatory and command-and-control approaches to employee rule-following. The results of this analysis confirmed that, as predicted, the self-regulatory approach prevailed over the command-and-control approach in facilitating deference and for preventing rule-breaking. Contrary to predictions, however, the influence of the command-and-control approach actually exceeded that of the self-regulatory approach in shaping compliance. This was the only finding which did not replicate the support for our predictions found in study one. However, the key reason we conducted study two was to test our predictions using supervisor ratings of employee rule-following. Regression analyses and structural equation models similar to those conducted on the self-report data were therefore conducted using the supervisor ratings of behavior that we collected. The results of these analyses are presented in Table 2.

Implications Traditionally, organizations have subscribed to a belief that the only way to get employees to follow organizational rules is to monitor them and then reward or punish them, depending on whether they did indeed follow the rules or not. Such an approach can get employees to fall in line with organizational expectations, at least to the extent that monitoring systems are extensive and reward/punishments sufficiently large. However, our studies show that this approach generally has a weaker impact on rule-following than the self-regulatory approach we have outlined and tested. Companies may thus have a great deal to gain by going beyond conventional instrumental strategies of social control. Further, not only is the self-regulatory approach to employee rule-following more effective, it is also more efficient, since employees take the responsibility of following rules on themselves. This leads to a reduction in the command-and-control strategy’s tangible costs as well as the intangible toll of polluting the employee/employer relationship. In turn, the self-regulatory approach allows organizations to devote greater organizational resources to uses that are more central to the achievement of organizational goals. It also enables organizations to more easily gain the loyalty and commitment of employees. The more general point is that the development of intrinsic motivations among employees begins at the top, with the leadership of the organization. When upper management does not itself conform to ethical codes of conduct, as appears to have been the case in several recent corporate scandals, the legitimacy of those authorities is eroded and the perceived congruence of values between the employee and the organization is diminished. But when the leaders of the organization appeal to employees’ value systems and present themselves as deserving of the power they hold, new approaches to fostering employee cooperation become viable and superior routes to organizational success emerge.

Steven L. Blader is assistant professor of management and organizations at NYU Stern. TOM R. Tyler is professor of psychology at New York University. The research discussed in this article is drawn from an article that will appear in an upcoming issue of Academy of Management Journal. |

Such problems raise the question of whether there might be an alternate

strategy for gaining employee adherence to organizational rules.

We have been conducting research exploring just such an alternative:

the self-regulatory approach. Rooted in social psychological research,

the self-regulatory approach argues that employee rule-following

can be best achieved by activating an intrinsic desire by employees

to follow organizational rules. Rather than relying on extrinsic

factors such as incentives and sanctions, our self-regulatory model

argues that the key to employee rule-following is to design organizations

that lead employees to intrinsically want to follow organizational

rules. In such an environment, employees do not need to be coerced

into following rules through the provision of incentives and sanctions.

Such problems raise the question of whether there might be an alternate

strategy for gaining employee adherence to organizational rules.

We have been conducting research exploring just such an alternative:

the self-regulatory approach. Rooted in social psychological research,

the self-regulatory approach argues that employee rule-following

can be best achieved by activating an intrinsic desire by employees

to follow organizational rules. Rather than relying on extrinsic

factors such as incentives and sanctions, our self-regulatory model

argues that the key to employee rule-following is to design organizations

that lead employees to intrinsically want to follow organizational

rules. In such an environment, employees do not need to be coerced

into following rules through the provision of incentives and sanctions.