![]()

|

But with each passing year, the power of such assets to generate new wealth may be declining. In fact, physical and financial assets are rapidly becoming commodities, which yield at best an average return on investment. Increasingly, economic wealth and growth lie in, and are driven by, assets that are more intangible – brands, software, patents, business models, organizational systems. If you really want to hit it big in the 21st century, don't head to California in search of gold or oil. Instead, go to Silicon Valley and establish a dominant competitive position, nail down a temporary monopoly, or create a compelling brand – by writing pioneering software, like Bill Gates, or by developing an innovative business model, like Jeffrey Bezos of Amazon.com. In recent years, intangibles have come to loom ever larger in the consciousness of managers and investors. Unfortunately, when it comes to intangibles, our business infrastructure is behind the times. The traditional accounting system is not equipped to reflect the value and performance of intangible assets. Investors systematically undervalue the shares of intangibles-intensive enterprises, particularly those that have not yet reached significant profitability. The rise of intangibles renders some traditional financial information and metrics less relevant. And the confusion can lead to both increased volatility and the manipulation of financial information through intangibles. The astonishing rise – and even more astonishing implosion – of Enron, a tangible asset (pipelines and power) company that turned itself into a supercharged intangible asset company (bandwidth and energy trading platforms) serves as a dramatic case in point. There is a great deal of confusion surrounding the use and abuse of intangible assets. And since I've spent portions of the last several years thinking, writing, and talking about intangibles, I thought it would be useful to offer a primer of sorts on intangibles. What are Intangibles? Merriam Webster's International Dictionary defines intangible as "incapable of being defined or determined with certainty or precision." I believe that intangible assets can be defined, but they cannot be determined with certainty or precision. Assets are claims to future benefits, such as the rents generated by commercial property, or cash flows from a production facility. Intangible assets are claims to future benefits that do not have a physical or financial embodiment. Patents, brands, or unique organizational structures – i.e. Internet-based supply chains – that generate cost savings are intangible assets. Different disciplines use different terms to identify such assets. Accountants refer to intangibles, economist calls them knowledge assets, and management and legal scholars prefer intellectual capital. When the claim is legally secured, like a patent, the asset is generally referred to as intellectual property. Intangibles are produced through three major methods – discovery, organizational practices, and human resources. The bulk of pharmaceutical giant Merck & Co.'s intangibles was obviously created by Merck's massive and highly successful research and development effort ($1.82 billion in 1998) aimed at discovering new products. In contrast, Dell's major value drivers are related to its unique organizational design – direct customer marketing of built-to-order computers via telephone and the Internet. Brands, a major form of intangible assets prevalent particularly in consumer products – think Sony electronics and Coca-Cola – are often created by a combination of innovation and organizational structure. Intangibles that relate to human resources are generally created by unique training, incentive-based compensation, and collaborative learning programs. Such initiatives can reduce employee turnover, provide incentives to workers, and facilitate the recruitment of highly qualified employees. Xerox's Eureka system, which allows the company's 20,000 maintenance personnel to share information, enhances the value of the human resource-related intangibles by increasing employee productivity. Of course, intangible assets are often created by a combination of all three sources. And it should be noted that the lines separating intangible assets and other forms of capital are often blurry. Intangibles are frequently embedded in physical assets (for example, the technology and knowledge contained in an airplane) and in labor (the tacit knowledge of employees). Why Do They Matter Now? Intangible assets are not a recent invention. Over the centuries, intangibles were created whenever ideas were put to use in households, fields, and workshops. Breakthrough inventions such as electricity, internal combustion engines, the telephone, and pharmaceutical products have created waves of intangibles. But starting in the mid-1980s, two related economic forces have driven a surge in the value and importance of intangibles. The first is intensified business competition, brought about by the globalization of trade and deregulation in key economic sectors such as telecommunications and financial services. The second is the advent of information technologies, most recently the Internet. These two developments – one economic and political, the other technological – have dramatically changed the structure of corporations. And a case study of Ford Motor Company, as told in Forbes, demonstrates precisely how these two trends have led to a greater focus on intangibles among twenty-first century businesses – and how business observers have come to speak the language of intangibles.

In April 2000, Forbes reported, Ford decided to return $10 billion to shareholders, "capital that would not be needed by the new, leaner Ford." The company was spinning off its parts plants into a new entity, called Visteon, which would supply Ford. As it shed physical assets, Forbes continued, Ford was boosting investments in "intangible assets." It paid $12 billion over the previous few years to purchase prestigious brand names like Jaguar, Aston Martin, Volvo, and Land Rover. "None of these marquees brought much in the way of plant and equipment, but plant and equipment isn't what the new business model is about," the magazine noted. "It's about brands and brand building and consumer relationships." Moreover, Ford was using the Internet to substitute "an outside supply chain for company-owned manufacturing," and to facilitate a "continuous interaction with consumers that offers myriad ways to enhance the brand value." Forbes concluded, as it wondered whether Ford could be the new Cisco, that "decapitalized, brand-owning companies can earn huge returns on their capital and grow faster, unencumbered by factories and masses of manual workers." The emergence of intangibles – like brands – as the major driver of corporate value at Ford is thus the direct result of the two forces mentioned above: competition-induced corporate restructuring facilitated by emerging information technology. Ford is not an aberration. Driven by severe competitive pressures, the rapid pace of innovation, and the deregulation of key industries, companies in practically every economic sector started in the mid-1980s to restructure themselves in a fundamental and far-reaching manner. Vertically integrated industrial-era companies, intensive in physical assets, had been designed primarily to exploit economies of scale. But, as Carl Shapiro and Hal Varian note in Information Rules, these production-centered advantages were ultimately exhausted and could no longer be counted on to provide a sustained competitive advantage in the new environment. Companies responded in two ways. One response was to deverticalize – to outsource activities like parts production, or payroll processing, that do not confer significant competitive advantages. The second was to strengthen the emphasis on innovation as the major source of sustained competitive advantage. These two fundamental changes in the structure and strategic focus of business enterprises gave rise to the ascendance of intangibles. Intangible Linkages and Human Resources The vertical integration of industrial-era companies is increasingly substituted by a web of close collaborations and alliances with suppliers, customers, and employees. These arrangements are facilitated by information technology, and particularly by the Internet. And they can help produce economies of network, in which gains are primarily derived from relationships with suppliers, customers, and sometimes even competitors. Such network economies can complement and sometimes substitute for traditional economics of scale. In the industrial era, linkages between different units were mostly physical and relied on tangible assets, like conveyor belts that linked auto parts divisions to railroad networks. Today, the essential linkages between firms and their suppliers and customers are mostly virtual and rely upon intangibles. Examples include Cisco's web-based system of product installation and maintenance; Merck's one-hundred research and development (R&D) alliances; and Wal-Mart's computerized supply chain. These highly valuable intangibles, often termed organizational capital, were not major assets before the 1980s. The highly connected twenty-first century corporation is also more dependent on its employees than its industrial-era predecessors. Economic developments have considerably weakened firms' control over human resources, as skilled employees enjoy greater alternatives. With easier access to financing, employees have far greater opportunities to leave and start their own companies, or to join other start-ups. Amar Bhide found in The Origin and Evolution of New Businesses that some 70% of the firms in the Inc. 500 list – a group of young, fast-growing companies – were established by persons who replicated or modified innovations developed within their former employers. Meanwhile, as University of Chicago professor Luigi Zingales has noted, the expansion of global trade has opened the door for independent suppliers. The increasing rate of employee turnover in many sectors highlights the deteriorating bonds between employers and employees. Obviously, firms that are able to maintain a stable labor force and reap a significant portion of the value created by employees possess valuable employee-related intangibles. Specific training programs, compensation practices such as substantial stock-based compensation awarded deep down the corporate hierarchy, and efforts to establish entrepreneurial centers within corporations help stabilize the work force. Like organizational capital, such employee-related intangibles were not prominent in industrial-era enterprises. The Urgency to Innovate Innovation has always been an important activity of both individuals and business enterprises. The prospects of abnormal profits or monopoly rents, protected for a certain period by patents or "first-mover advantages," have always provided strong incentives to innovate, whether it was Thomas Edison and Edison Electric in the 1880s or Bill Gates and Microsoft in the 1980s. The difference between then and now

is the urgency to innovate. Given the decreasing economies of scale

and ever increasing competitive pressures, innovation has become a

matter of corporate survival. Accordingly, there has been a sharp

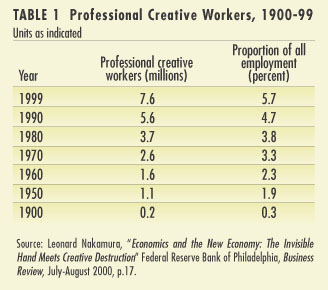

increase in the number of professional workers engaged in innovation.

As shown in Table 1,

during the first 70 years of the twentieth century the number of creative

workers rose by 2.4 million; during the next thirty years the number

rose 5 million. Note also the corresponding increase of creative workers

in proportion to all employees, from 3.8 % in 1980 to 5.7 % in 1999. Many nineteenth- and early twentieth-century innovations were made by individuals and were subsequently developed by corporations – the telephone, electricity, and the television, to name a few. But in the past 50 years, innovation became a major corporate activity. In 1998, U.S. corporate expenditures on R&D, one of several forms of investment in innovation, reached $145 billion. Even in traditional industries, success and leadership can now be secured only by continuous innovation. Wal-Mart, with its state-of-the-art inventory management system, and Corning, which translated expertise gained in producing housewares into producing fiber-optic cable, are prime examples of this trend. The new products, services, and processes generated by the innovation process (new drugs, automatic teller machines, Internet-based distribution channels) are the outcomes of investment in such areas as R&D, acquired technology, and employee training. When such investments are commercially successful, and are protected by patents or first-mover advantages, they are transformed into tangible assets creating corporate value and growth. Who Should Care? There are several groups of professionals who should take a particular interest in the implications of the rise of intangibles. They include: Corporate managers and their shareholders. Evidence indicates that intangible investments are associated with excessive cost of capital, beyond what is called for by the higher-than-average risk of these investments. The excessive cost of capital, in turn, hinders investment and growth. Investors and capital market regulators. Research has documented in intangibles-intensive companies the existence of an above-average gap in information about firms' fundamentals between corporate insiders and outsiders. Economic theory suggests that such large and persistent information asymmetries between parties to a contract or a social arrangement lead to undesirable consequences, such as systematic losses to the less informed parties and thin volume of trade. Accounting standard setters and corporate boards. Empirical evidence indicates that the deficient accounting for intangibles facilitates the release of biased and even fraudulent financial reports. This should obviously be of concern to the Securities and Exchange Commission, the Financial Accounting Standards Board, and to corporate board members who rely heavily on accounting-based information to monitor managerial activities. Policymakers. The various intangibles-related deficiencies in financial information adversely affect public policymaking in key areas. These include areas of fiscal policy like the research and development tax incentive, the optimal protection of intellectual property, and the desirability of industrial policy. The Future of Intangibles In the wake of the sagging stock market, the current recession, and particularly Enron's debacle some critics have been quick to proclaim the end of the New Economy, which was built, in large part, on intangibles. Since I never joined the New Economy-Information Revolution fan club, I do not feel compelled to participate in the current soul searching brought on by the bursting of the technology bubble. I am concerned, however, that intangibles – to which I have devoted much of my research and professional activities in recent years – will be swept by the tide of disillusionment and ridicule surrounding the New Economy. I am concerned that people will lump together the permanent phenomenon of intangible investments as the major source of corporate growth and value with transitory economic downturns, stock market volatility, and the financial difficulties currently encountered by certain technology sectors. And that the exaggerated, often unfounded claims about technological revolutions and new business models, now in disrepute, will overshadow real and fundamental economic developments in which technological change and innovation, ushered by intangible investments, play such a major role. But the trends that have powered the growth in intangibles – global competition and increases in the use of information technology – have not been negated by the bursting of the .com bubble. Surely, the rate of intangible investment may be affected, to some extent, by economic circumstances and capital market conditions. But intangibles will remain central to corporate success, economic growth, and the enhancement of social welfare – whether the NASDAQ is at 2000 or 6000. Pharmaceutical and biotech companies will continue to direct most of their resources toward intangible investment in scientific discoveries and drug development; chemical companies will continue to devote significant capital to develop new products. Retailers with their razor-thin margins and transparent prices will create value by expanding online operations and instituting improved supply chain processes. Financial institutions will grow mainly through creating new products and improved customer relations. Old Economy or New Economy – it doesn't matter which – an enterprise's competitive survival and success will primarily depend on smart intangible investments leading to innovation and effective commercialization. Economic slow-downs and capital market declines do not change these fundamentals. What is changing, though is the urgent need to gain a thorough understanding of the role of intangible capital – along with tangible and financial assets – in the process of value creation by business enterprises, to improve managerial processes for coping with the idiosyncratic challenges posed by intangibles, and to develop measurement and valuation tools for both managers and investors. In the fall of 2000, an article by New York Times columnist Paul Krugman may have articulated the central challenge facing us: "The intangibility of a company's most important assets makes it extremely hard to figure out what the company is really worth." In the booming economy and roaring capital markets of the 1990s, crude measurement and valuation models could be tolerated, at least for a while, and speed and agility carried the day. But in today's environment, with its slow-growth economy and stagnant capital markets, managers and investors must adopt different mindsets when it comes to intangibles. Managers must pay meticulous attention to corporate resource allocation. In particular, they should develop the capability to assess the expected return on investment in R&D, employee training, information technology, brand enhancement, online activities, and other intangibles and compare these returns with those of physical investment. Managers should also continuously monitor the efficiency of intangible asset deployment. Licensing patents, for example, may not be a top priority when earnings are ample, but they can be an important source of income during periods of slow growth. Human resource practices, such as incentive-based compensation, require careful planning and monitoring when the going is tough. At this time, most business enterprises simply do not have the information and monitoring tools required for the effective management of intangibles. Investors must change their mindset, too. Superficial investment analysis with a focus on short-term corporate earnings will no longer suffice in a volatile but generally flat stock market. The crude valuation models currently used by most analysts lack the capability to provide early warning signals of impending problems and will have to be replaced by an in-depth analysis of the enterprise's business model, with a focus on the capacity of the firm to learn, innovate, and secure maximum benefits from products and services. A continuous assessment of managers' deployment of intangible and tangible resources will have to precede and underlie the current prediction of next quarter's earnings. In short, in this climate, I foresee a need for both managers and investors to pay more, rather than less, attention to intangibles. In doing so, The emphasis, however, should shift from superficial cliches like the New Economy to serious analysis of the economics of intangible assets and their role in corporate value creation and the enhancement of social welfare. It is now time to move from exclusively dealing with "low-hanging fruit," such as patent licensing and intranet systems, to the full incorporation of intangible capital in the managerial strategic and control processes; and from essentially ignoring key intangibles (human resources, in particular) in the analysis and valuation of investments to fully recognizing their role in corporate value creation.

Baruch Lev is Philip Bardes professor of accounting and finance at NYU Stern and chairman of the Vincent C. Ross Institute of Accounting Research. This article is adapted, with permission, from his book, Intangibles: Management, Measurement, and Reporting (Brookings Institute Press).

|

||||||||||||||||||||||||||||||||||||