![]()

|

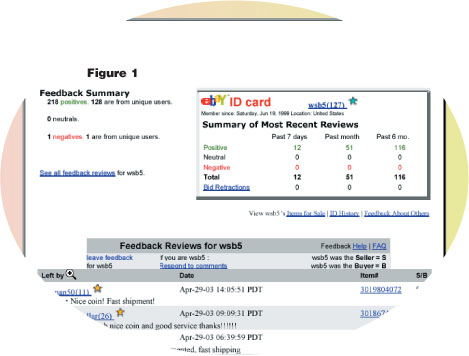

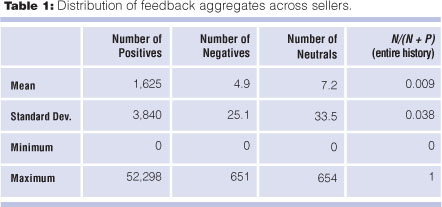

After an auction is completed, buyers and sellers can give one another grades of +1 (positive), 0 (neutral), or -1 (negative), and add textual comments. EBay then displays several aggregates of the grades: the overall rating, the sum of positives minus negatives received by a seller; the percent of positives; the date when the seller registered; a summary of recent reviews from the past week, month, and six months; and the entire feedback record, an exhaustive list of reviews left for the seller. With its well-defined rules and mass of available information, eBay thus presents the researcher with a fairly controlled environment for theory testing. So we decided to use this data to investigate how feedback comments affect reputation, future sales, and the willingness of eBay participants to continue buying and selling goods. The average seller in our sample has 4.9 negative feedback points, corresponding to 0.9 percent of all comments. The maximum number of negative feedbacks received by a seller is 819, but this seller took part in 52,298 transactions. The median seller in our sample has only one negative feedback, and more than a quarter of the sellers have none. Our subjective impression, after browsing through eBay community chatboards, is that the information contained by a neutral rating is perceived by users to be much closer to negative feedback than positive. Given this, we decided to lump negative and neutral comments together when talking about “negative” comments.

Negative Feedback and Sales

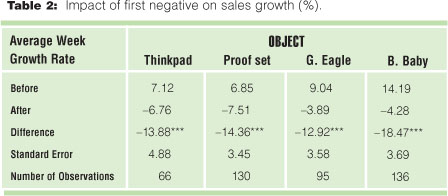

Frequency of Negative Feedback We next examined whether the arrival of the first negative rating has an impact on the frequency with which subsequent negative ratings are given. We measured time in two ways: number of sales transactions and calendar time (number of days). For the Thinkpad, it takes on average 129 transactions before a seller receives his first negative, but only 60 additional transactions before the second arrives. Similar results are obtained for the other three objects. When we replicated this analysis with time measured in days, the difference between the interarrival times of the first vs. the second negative is again quite striking. In the Thinkpad market, for example, it takes on average 300 days for the first negative to arrive, but only 66 days for the second one. In all cases we considered, the increase in frequency after the first negative is statistically significant. By contrast, the arrival of the second, third, up to fifth negative seems to have no impact on the frequency of negative feedback.

At the very least, it appears from these results that there is something special about the first negative that a seller receives: Once the first negative arrives, the second one arrives faster. Given the significance of this result, both in statistical and in economic terms, we set out to find possible explanations. One explanation is that buyers have a threshold of dissatisfaction above which they give a negative, and that this threshold drops after the first negative. There are several behavioral mechanisms through which this can happen. There could be a decrease in the cost of writing a negative comment. Many negative comments from buyers are followed by a retaliatory negative comment given by the seller; and seller retaliation might impose an economic cost on the complaining buyer, especially if the buyer is also a seller. Such an effect would confound our results if the probability of retaliation by a seller in reaction to her first negative is higher than retaliation to her second negative, an explanation proposed by several eBay users we talked to. In order to investigate this possibility, we checked whether each particular negative comment by a buyer was accompanied by a retaliatory negative left by the seller. The result was striking: Of the almost 10,000 negative/neutral instances in our data, 2,462 resulted in a retaliatory comment by the seller. However, our data indicates that sellers are not more likely to retaliate upon their first negative, as opposed to subsequent negatives. So it does not appear that “fear of retaliation” is a significant driver of the difference in interarrival times of negative comments.

Next, we considered the possibility that buyers are influenced by other buyers’ behavior. In particular, faced with poor performance by a seller with a perfect record, a buyer might be inclined to think that there is no ground for a negative feedback. For example, if there is a communication problem between buyer and seller, the former may attribute this to a problem with him or herself. However, if the seller has already received a negative feedback, especially regarding the same problem that the buyer is now facing, then the buyer may have a greater inclination to attribute this to a problem with the seller. To consider this possibility, we classified the first and second negative remarks according to their nature. The buyer-influence story should imply an increase in the relative importance of subjective problems in second negatives. However, the results suggest a very similar pattern for first and second negatives. Moreover, “item never sent,” arguably the most objective reason for negative feedback, actually increases in relative importance (though by a small amount). At the opposite extreme, “bad communication,” arguably the most subjective reason for negative feedback, also increases in importance (though by an even smaller amount).

Finally, if the “threshold” story holds true, we would expect the comments accompanying first negatives to be nastier than the comments accompanying the second and subsequent negatives. In order to test this possibility, we created pairs of comments corresponding to each seller’s first and second negative. We then asked a third party (a student) to make a subjective evaluation as to which of the two remarks was more negative. (We randomly mixed the order of the comments so that the student could not tell which was the first and which was the second negative). The results show that 51 percent of the second negatives were considered nastier then the corresponding first negative, a split that is not statistically different from 50/50. In sum, the empirical evidence suggests that the behavioral change from the first to the second negative is not due to changes in buyer behavior, but rather to changes in the seller behavior. Our interpretation is that, once the first negative arrives, a seller’s reputation is worth less and the value of protecting such reputation is also lower. Accordingly, the seller makes less effort to guarantee a good transaction and as a result more negative feedback experiences take place.

Reputation and Exit Next we considered the possibility of a seller “exiting,” i.e., secretly changing his identity and starting a new reputation history. Intuitively, we would expect the seller’s tendency to do so to be decreasing in the seller’s reputation. We supplemented our data set by revisiting our sample of sellers in the first week of January 2004, and checking whether they were still in business. Of the 819 sellers originally sampled, we found that 152 had not conducted any transactions within the last 45 days and 61 sellers had not sold anything within the last 45 days, but had bought an item. We also could not locate the feedback records for 104 sellers in our sample, since eBay’s database claimed that these seller IDs were no longer valid. In summary, our data is consistent with the possibility of opportunistic profit-taking and exit behavior by sellers. There are, however, alternative stories consistent with the data. For example, it might be that some unexpected exogenous event leads the seller to offer poor service for a period of time, which results in an increase in negative feedback, which in turn results in the seller’s decision to exit (given such a poor record).

Buying a Reputation Casual observation of feedback histories suggests that many sellers appear to start out as buyers, completing a string of purchases before attempting their first sale. As can be seen from Figure 2, bearsylvania – a Beanie Baby dealer – started out as a buyer first, and quickly changed the pattern of his transactions from purchases to sales. We then defined a seller as having switched from being a buyer to being a seller if more than 50 percent of the first 20 comments referred to purchases, and more than 70 percent of the last 20 comments referred to sales. We found that 38 percent of Beanie Baby sellers, 22 percent of laptop sellers, 31 percent of gold coin sellers, and 31 percent of proof set sellers followed the “buy first, sell later” strategy. We also found that, on average, 81 percent of a seller’s last 20 transactions were sales, compared to 46 percent of the first 20 transactions. These results show that “buying first and selling later” is a widespread phenomenon on eBay. Next, we investigated the correlation of the “buy first, sell later” indicator variable with the percentage of negatives in a seller’s record, as well as the length of the seller’s record. This regression suggests that a 1 percent level increase from the mean value of 0.7 percent of negatives to 1.7 percent of negatives is correlated with a 6.4 percent decrease in the probability that the seller switched from being a buyer to a seller. So although we do find indisputable evidence for the existence of switching behavior on eBay, our evidence for a clear economic incentive to do so is weak.

Conclusion The marketplace can be quite efficient in meting out punishment for those who don’t adhere to expected norms. On eBay, a vast marketplace itself, the reputation mechanism plays the role of punishing poor performance and behavior. Indeed, it is clear from our research that eBay’s reputation system gives way to noticeable strategic responses from both buyers and sellers. That is, the mechanism has “bite.” Of course, this does not imply that the current structure of the system is optimal. In fact, we believe an exciting area for future research is precisely the design of an efficient reputation mechanism.

LuÍs Cabral is professor of economics at NYU Stern. Ali Hortasçu is assistant professor of economics at the University of Chicago.

|