![]()

|

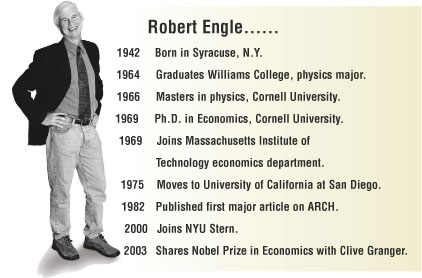

Dean Thomas Cooley: It's a good thing when good things happen to deserving people, and when your friends and colleagues get recognized for their accomplishments. We are just overjoyed at the great news that we all got this fall. Bill Greene: I'm going to throw Rob some easy questions and then I'll turn this over to the audience to follow up. So let me begin with the easiest ones of all. Can you tell us a bit about yourself and where you come from? Robert Engle: I grew up in Philadelphia. And I was an East Coaster for many, many years. My Ph.D. is from Cornell, where I went to study physics and then changed my mind. I actually taught at the Massachusetts Institute of Technology when Tom [Cooley] and I knew each other. And then in the mid-1970s, I went to the University of California at San Diego, and spent 25 years there. I came back east to Stern in 2000. Greene: Why economics and not physics?

Engle: Well, when I got to graduate school, I joined the laboratory studying superconductivity. It was in the basement of the physics building, and the only people you ever saw were a few other graduate students. I just decided I wanted to do something that had a little wider relevance. And I wanted to switch into a field that used some of the same ways of thinking that physics does. That's one of the reasons I switched to economics – and particularly why I became an econometrician. The best physics, of course, has both empirical work and theory. And I think econometrics provides exactly that intersection for economics. Greene: So where were you when you got the call? Engle: Well, you probably noticed that I haven't been here this fall. That's because I’ve been on sabbatical in France, in a town called Annecy in the French Alps. I had just been out to lunch with my wife, when I went out to do an errand and she came back to the apartment and got the phone call. The woman on the other end said, "Tell him that this is a very important call from Stockholm." And when the phone call came in again, the connection was not clear. The head of the Nobel committee has a relatively thick Swedish accent. Eventually I came up with the inference that yes, it was indeed that I had won the Nobel Prize. And I won it with my long-time colleague, Clive Granger from San Diego. The head of the committee said, "Your life will not be the same again; the press will be all over you." So when we hung up, we looked at each other. And here we are in this little medieval town in France. First of all, how did anybody ever find that phone number? But second of all, is the press really going to find us? Some of the press found us, but not too much. But mostly it was phones ringing in our home, in my office, and a lot of e-mails. I must have received hundreds of e-mails that day. Greene: The New York Times had an article a few days ago, in which they described econometrics as a rarefied field. But seven Nobel Prizes have been given to econometrics. Why do you think they have such an interest in this field? Engle: Econometrics is the tool. And in some ways, at its best, it is really what economics is about. I think it is a way of trying to make sense out of the world around us. The world around us is the data. And an econometrician is a person that looks at the data. Greene: Well, let's turn to your work. What is the contribution that you made that got the prize committee's attention? Engle: The prize citation says it is for “models of time varying volatility, parentheses ARCH.” Now they didn't tell you what ARCH stands for. I will, but only if you promise not to be put off by what it really stands for. It stands for Autoregressive Conditional Heteroskedasticity. If you take my class, I'll teach you how to say that, but other than that, it's just ARCH. It’s a way of trying to model, describe and forecast this thing we call volatility. In financial markets, we're so interested in the volatility of asset prices. Because when stock prices wiggle around, your portfolio can go up or down. And volatility is an important consideration as to what we can expect as you go forward in our portfolio. So the prize was for developing new methods for analyzing volatilities, which change over time. And the applications are pretty widespread. Greene: And this work began when you were in the U.K., studying inflation. How did you make this transition to financial markets?

Engle: Well, I was trying to solve a macroeconomics problem when I came up with the ARCH model. I was living in London as a visitor at the London School of Economics. And every day, I'd go to lunch with David Hendry and Jim Durbin and Dennis Sargan, and all these famous econometricians. And we talked about these models. But what I really wanted to address was the following question: Is the uncertainty in inflation an important determinant of business cycles? Milton Friedman had argued that it was. So I wanted a method that would look at the volatility of inflation. But the method we developed didn't really work very well in macroeconomics. It didn't explain things like business cycles or consumer spending very well. So it was considerably later that the finance applications really surfaced. In finance, we study how much risk you’re taking and what you’re getting for it, the tradeoff between risk and return. And this is a way of scientifically measuring the risk part of this equation. Greene: How do researchers use these techniques? Engle: Well, in a lot of different ways. When you try to calculate what can go wrong with a financial portfolio, or how you can diversify to reduce risk, you can look at the volatility. So one direction is how you can form optimal portfolios. And once you have evidence about how volatilities are changing over time, some dynamic portfolio strategies that make sense may emerge. Another important application is in measuring what's called value at risk, which is how much your portfolio might go down in the next day. A third application, which is quite closely related, is the pricing of derivatives and options. Options can function like insurance contracts to protect against declines in your portfolio. But what is the fair price for this kind of insurance? And the answer, of course, depends on how volatile your portfolio is. Greene: Can individual investors use these techniques? Engle: Institutional investors do this every day. Institutional investors calculate the value at risk, not only of the company as a whole, but of their fixed income portfolio, and of their Japan portfolio, and of their yield portfolio. So there is a very scientific approach to calculating risk in an investment bank. But individual investors do not very often build ARCH models. I would think it would make a lot of sense, when you have a brokerage accountant at Merrill Lynch or Charles Schwab, to be able to use their standard software and calculate the value at risk every day. The individual investor could really look at that. It would help them realize whether the market is getting more volatile and whether they might want to shed some risk, just like an institutional investor. Greene: What are you working on now? What's next?

Engle: Well, there are two directions that these models are going that I'm very interested in. First, instead of just talking about volatilities of one asset at a time, or one portfolio at a time, I’m interested in looking at many assets at once. The multivariate extension of this has been a problem for many years. There’s no widely accepted multivariate model. But I have a candidate. I gave a lecture series on this at Erasmus University last summer, and I'm writing a book about it for Princeton University Press. The other direction is to use higher and higher frequency data. We often look at these models once a day or once a month. But really, every time there is another transaction or another price quoted, you could update your volatility model. And that has lots of implications for trading.

Audience Questions: Question: Clearly inputs to the Black-Scholes options pricing model assume that volatility is constant. How does ARCH and ARCH models alter that or update that model?

Engle: Right, well, that's absolutely right. The Black-Scholes model is based on the assumption that volatility is constant. And yet practitioners, of course, know it's not. So Wall Street has figured out a solution. They talk about implied volatilities, and watch how they change. So a simple answer is that over time, you would keep updating your ARCH model and forecast what the volatility would be. And you could use that as an input to the Black-Scholes formula. More sophisticated methods would change the formula. Question: Do you think that the extension of your model will finally apply to macroeconomic data? Engle: I didn't mean to say that it didn't apply to macroeconomic data now. When you apply these models to macroeconomic data, you get an interesting interpretation. It turns out that the way you think about it is that if you're going to make macroeconomic forecasts, just like you forecast the stock price, there’s going to be some uncertainty surrounding it. That's what we call the uncertainty, or the volatility. When you forecast a macroeconomic variable, like Gross National Product, or something like that, we've got a confidence band around that. We've got some measure of uncertainty. And the ARCH model is a way of measuring that uncertainty. What we've learned is that by any reasonable way of looking at it, macroeconomic uncertainty seems to be going down all the time. The macroeconomic aggregates seem to be more predictable than they used to be. And so it's sort of like we've got better and better measurement tools for seeing these things. That's not the case in finance. And if you did this as a multivariate problem in macroeconomics, I'm sure you'd see the same sort of thing. But you would also see correlations between errors that you make in forecasting inflation, and errors that you make in forecasting unemployment.

Engle: When I discovered this ARCH concept, I did think it was a good idea. But it wasn't that easy to get it published. I had to do a lot of revisions and arm wrestling with the journals. But I had no idea that it would be this good an idea. What made it turn out to be an idea that had such mileage in it? I think it was the applications that I didn't think about – the applications in finance. There was a paper published in '87 by French, Schwert and Stambaugh, which applied these methods and some alternative methods to financial data with lots of implications. This was published in the finance community. And all of a sudden, there was a whole lot of new interest in this model. I can't say that I had any idea that it would have this kind of audience, because I didn't really recognize that finance was a natural place for it. So I guess I was just lucky. Question: Can you talk a little bit about the time you came up with ARCH? What was the process like just before the model cohered? Engle: Yeah, I'd like to do that, actually, because it's sort of fun to try to reconstruct. I think there were three inputs to this model that were really important. One was I was interested in this macroeconomic problem. I was concerned about rational expectations and all these kinds of things. And I thought maybe uncertainty was the missing item that would make the macro models work. I knew what I wanted the model to do, but I didn't know how to do it. The second input was I had been doing a lot of work on a way of writing probability density function of a variable, in terms of its past. If we’re talking about random events, what’s the distribution of the random outcomes tomorrow, conditional on what we know today? And this turns out to be a very powerful way of thinking about dynamic processes. Whenever you're trying to forecast something, one of the hard parts is figuring out where you are today. So a conditional forecast is a really important thing. And so this is an idea that had made a lot of progress in macroeconomic forecasting, when the big models had been beaten by simple time series models, because they took better account of the conditional forecasts. Then there was a third input. Before I left San Diego, I was doing something on the computer, and Clive Granger came into my office, and he said that he was interested in a new test statistic, which was to square the residuals from some kind of a regression model, and look at the autocorrelation of these square residuals. And he had proposed this as a test statistic for a bilinear model. Bilinear models are pretty esoteric models in statistics. And he had proposed this test. And he said, "See, I'll show you it works." Square your residuals and fit this autoregression. So I squared the residuals of this little model, fit the autoregression, and it was very significant. And I thought, "Oh, my goodness, isn't that amazing. This really works on real data." But in the back of my mind, I thought even at the time, I don't think this test is a test for a bilinear model. What is this test really a test for? And so when you know what the data looks like and you know what the test is, you can sometimes reverse engineer it and ask what model this test is good for. And that was the third piece. When those three pieces came together, that was the ARCH model. Question: Can you tell us about what brought you to NYU? Engle: Yes. This evolution in my interest from macroeconomics to finance meant that I was continually working in areas where I didn't really have colleagues, and where I was pretty far away from financial markets. So I was actually very anxious to have the kinds of excellent colleagues that I have here. Stern has a great finance department and the faculty is interested in all sorts of areas of finance, many of which I didn't know very much about. And so when you think about what I said the applications are – risk management, derivatives pricing, asset allocation – there are experts in all those areas in the department. So it was a great connection for me to come here. The first time I came to Stern was as a visiting professor for a semester, and then I went back to San Diego. And then I decided to come permanently. When you're studying financial markets, you can't do any better than to be in New York. They're all around here. One of the great things is teaching MBA students who have this great expertise in whatever their job training was. And it's fascinating to teach people who know the innermost details of some of these markets. That wasn’t the case in San Diego. So it's been a lot of fun for me being here. |

Question: When you came up with the ARCH concept in 1980 or so, did

you ever think it would lead eventually to this?

Question: When you came up with the ARCH concept in 1980 or so, did

you ever think it would lead eventually to this?