![]()

|

We set out to investigate some of these claims by using the tools of modern macroeconomics. We set up a model of how an economy looks and functions when on its long-term growth path. And then we analyzed how that economy would change when an information technology revolution hit. In addition, we examined some concrete historical data to measure the extent to which some of these hypotheses have been borne out. To understand the background of the debate over the existence of the New Economy, we first need to understand the role of information and its availability in the economy. Information is a central attribute of goods. The key feature of information is that, once it is produced, it can be used repeatedly with little additional cost. Software that costs hundreds of millions of dollars to develop can be copied on a CD for a few cents. Similarly, a $100 million sports event – an NBA final or a World Cup soccer match – can be enjoyed by an additional sports fan with almost no extra cost. Because the production of information itself is human-capital intensive, in an information age, human capital will become a more important determinant of economic success. Indeed, human capital investment decisions play an important role in the nature of the goods that are produced and have important implications for the distribution of income.

Information is, in effect, a key component of the production process. And different goods have different levels of information content. Goods are produced with two types of intermediate input: information inputs and non-information inputs. Information inputs have a marginal cost of zero, while the cost of non-information inputs is always non-zero. This framework implies a very broad notion of information. Essentially anything that once produced can be reproduced costlessly is information. For our purposes books, databases, software, magazines, music, stock quotes, Web pages, and scientific knowledge are all information. It is obvious that in an information age, information will become more important than other bricks-and-mortar inputs, and will become a larger part of consumption goods. We can also characterize all products in terms of their information intensity. Consider, for instance, the production process for delivering knowledge by teaching. Teaching involves non-information inputs like buildings and equipment that need to be provided to a marginal student at a positive marginal cost. The teaching activity itself, though, is an information input that is performed once, regardless of the number of students in a classroom or on a network. When one considers the shares of information and non-information inputs in the total cost of teaching, the share of information inputs (cost of teachers) outweighs the share of non-information inputs. So teaching is information intensive. In an information age, when access to students is less limited by the need for physical inputs, the information intensity of teaching increases. In contrast, for goods such as consumer durables and producer durables – i.e. washing machines or machine tools – a larger portion of total inputs is likely to be non-information intermediate inputs. Accordingly, the manufacture of these goods is a less information intensive production process. Long Term Growth What does a stable, growing economy look like before an information revolution hits? In this so-called steady state, the prices of new products decrease as they get older because the imitation cost declines through time and patent rights disappear. The patent owner prefers higher volume rather than a higher price as more and more people can afford it. In the steady state, the average age of products people consume changes across income levels. Those in the lowest percentiles of its income distribution consume a subset of older products. In this model economy, only agents above the 27th percentile have enough income to buy newer products. In equilibrium, newer goods are more expensive and they include a larger patent fee in their price. The patent fee paid to the patent owner, in turn, covers the product development cost. Agents who consume newer products with higher patent fees in them are thus making the product development investments for the whole society. Conversely, those in the lowest percentiles essentially pay no product development costs. In this example, approximately 24% of the total consumption expenditures of the richest 1% goes to pay the product development costs for the entire society. This economy grows along a balanced path, creating innovation and wealth at a predictable rate. Throughout history, of course, there have been periods when unexpected technological advances wrought fundamental economic and social transformations. In the past 30 years, of course, there has been just such a breakthrough. This time it came in the technology of information production. And the events of the past few decades raise the question: How does an information revolution alter or change the dynamics of a growing economy? More Innovation First, we would expect to see an increase in innovation. When the breakthrough in information technology occurs, agents realize that providing information-intensive goods to the market will be cheaper in the future. And that creates an opportunity to make more profits from the ownership of patents on high-information goods.

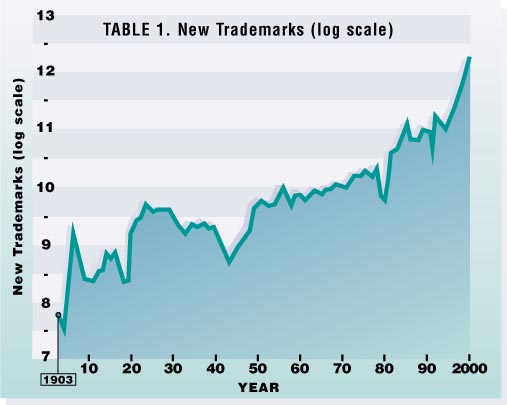

One way to document the growth of innovation is by looking at investment in new product development. In our model, the ratio of investment in new product development to output should rise from an initial level of 5.5% at the beginning of the breakthrough to above 15%. This high level of investment would continue for nearly 20 years, after which it falls back to its initial steady state level. These large investments in new product development cause the growth in the number of new products to surge from an initial 1.5% level before the breakthrough to more than 7% after the breakthrough. Most of the new goods introduced will be information-intensive goods. When we examine recent data, it is clear that the so-called New Economy of the past several years has been characterized by a dramatic increase in the number of new products. One way of quantifying innovation is through trademark data. Trademarking a product or a service is a relatively costly and time-consuming process; businesses won’t bother to trademark products unless there’s a sufficiently high probability that it will distinguish the product from rival products. And a trademark right can last indefinitely if the owner continues to use it. Table 1 shows the number of new trademarks issued between 1903-1997 on a log scale. As seen, there was a significant period of growth both before and after World War I, and then a 20-year decline during the Great Depression and World War II. The number of new trademarks issued annually was relatively level until the 1980s, when it began to increase dramatically. By this measure, at least, innovation has risen sharply in the New Economy. Slowing Productivity Growth There are other economic consequences to the rise in innovation. New product development uses economic resources. The increase in the amount of labor allocated to new product development is an investment in future output and welfare. But conventional productivity measures do not take into account the investment in creating new information-intensive goods. And that leads to a conclusion that some might regard as counterintuitive. In our model, this dynamic leads to an observed slowdown in measured productivity – a slowdown in growth that could last for almost 20 years. After this temporary slowdown, however, the cost-lowering benefits of the breakthrough in information technology kick in, resulting a 20-year period of high growth in measured productivity. Eventually, measured productivity continues to grow at the initial 1.5% a year level. However the gains in measured productivity are permanent. Greater Inequality With the improvements in the high-information

goods, producers of these goods – agents with high human capital

– will become more productive as a group compared to the low

human capital agents who produce low information goods. Accordingly,

the income gap between these two groups will increase. In essence,

then, the efficiency increase in the distribution technology benefits

the highest output, highest income, highest human capital agents the

most. Given this, one would expect the income gap between the rich and the poor to widen after a technological breakthrough. Our model suggests that by the time 25 years have elapsed, the income gap between these two groups should increase by about 35%. And when we examine recent data, we see that beginning in the 1970s and continuing in the 1980s and 1990s, income inequality in the U.S. did increase dramatically. Similar patterns have been observed in other countries that are members of the Organization for Economic Cooperation and Development (OECD). Of course, some of this rise has been due to an increase in the wage premium for skilled workers. In a 1997 study, Jeremy Greenwood of the University of Rochester and Mehmet Yorukoglu linked this observation to an information technology revolution beginning in 1974 and noted that similar patterns were observed in previous industrial revolutions. Many analysts seem to have settled on the explanation that this rise in inequality across skill groups is largely due to skill-biased technical change. But there is a slightly different causal

interpretation of the rise in inequality that is linked to information:

the growth in winner-take-all markets. In 1981, the late economist

Sherwin Rosen predicted that new technologies, by increasing the scope

of the market for the most talented performers, would increase the

inequality of incomes. Another argument holds that information inputs

allow markets to expand in scope, and therefore the rewards for the

most successful competitors increase dramatically. Thus, the rise

in inequality is directly linked to growth in the information content

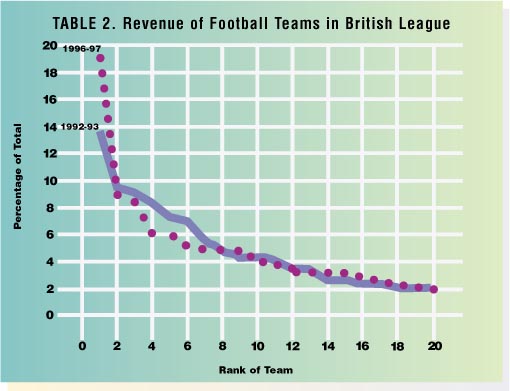

of goods. This dynamic can be seen in Table 2, which shows the revenues of teams in the British Premier Football League for the period 1992-1993 and 1996-1997. As seen, the most successful teams received an increasing share of the revenues. The change coincided with a change in this period of the information content of the product. A sports channel was introduced, which made the games of all teams more accessible to the viewing public. This increased the exposure of the most successful teams and resulted in their having a larger share of the revenues. Similar phenomena are prevalent in other professional sports and in many other markets. New Product Diffusion In this economy, the rich will consume

more than the poor. But that’s not the crucial distinction between

the consumption habits of rich and poor. What matters is that the

rich will consume the high price new varieties of goods that the poor

cannot afford. Over time, as the goods get older, the price falls

and the income of the poor grows to the point where they can afford

the newer goods. The welfare difference between the rich and the poor

naturally then depends upon how closely the poor follow the rich in

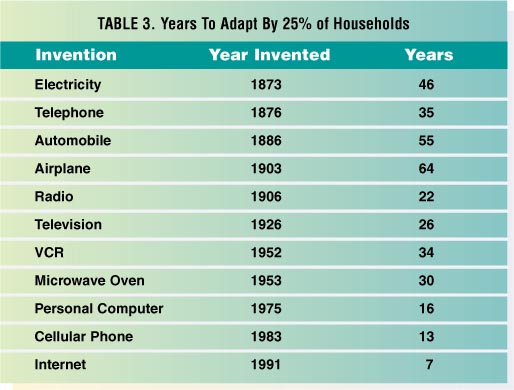

consuming new goods. After the information breakthrough, with the boom in new high-information goods, the average age of goods consumed by the rich falls. But as time goes on, the prices of high-information goods fall at a more rapid rate than the prices of low-information goods. (The price of software falls more rapidly over time than, say, the price of sneakers.) After a few years the price of high-information goods falls sufficiently that the poor can afford them. Once the economy converges to the final steady state, the gap between rich and poor is permanently narrowed. This dynamic would also result in the more rapid diffusion of new information intensive products into household’s consumption bundles. Table 3 shows the time elapsed from the date of important innovations to the point at which 25% of households have them as part of their consumption bundles. What is striking is that the time to adoption has declined dramatically for more recent innovations. It took 22 years for 25% of households to acquire radios, but only seven years for 25% of households to get online. Falling Prices As diffusion increases, prices for the

reproduction and distribution costs of information intensive goods

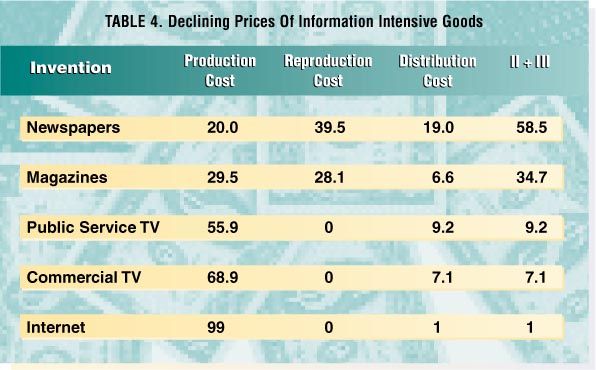

fall. Table 4 provides

estimates of the share of production, reproduction, and distribution

costs as a percentage of total cost for various types of media. By

definition these are all high information content goods. Reproducing

and distributing newspapers, a classic old media product, eat up 58.5%

of total costs. But reproducing and distributing data on the Internet,

the ultimate new media product, takes up just 1% of total costs. In part because of such declines, the prices consumers ultimately pay for information intensive goods also would be expected to fall in an economy affected by an information technology breakthrough. And that is precisely what has happened. For most categories of software – a highly information intensive good – the price declines very rapidly after its development. Between 1990 and 1997 the average rate of price decline for spreadsheets was around 29% a year not adjusted for quality improvements. In the same period the rate of price decline for word processing programs has been around 23% annually. The Poor Get Richer? The results so far have shown that an information revolution, by easing the constraints that prevent the more able from capturing a larger market and a bigger share of the pie, increases income inequality. Does this imply that the poor are made worse off? Well, yes and no. Welfare is calculated by figuring how much compensation as a percentage of income each group would require to be indifferent between being an agent in the information age and an agent in the extended path of the old economy – assuming continued productivity growth. Making these calculations enables us to measure how much better or worse-off each group of agents are made with the breakthroughs of the information age. Our model shows that the well-being of the rich increases sharply starting from the early days of the information age. After all, as producers of information intensive goods, they are becoming more productive with the improvements in the distribution technology. And they get to consume these new information toys right away. For those in the lowest decile of the income distribution, things do not change very dramatically at first. At the beginning the new information intensive goods are expensive and beyond the reach of the poor. The only benefit for the poor during the early years is that the old information goods are becoming cheaper. As time passes, the mass of new information intensive goods produced at the beginning of the information age become cheaper, and the poor start to benefit from them. After almost 20 years from the dawn of the information age, a long era of 30 years begins during which the welfare of the poor increases sharply. The increase is so dramatic that after 40 years or so the welfare gains of the poor outstrip those of the rich. It is important to note that the rise in welfare is due entirely to the fact that those in the upper tail of the income distribution paid the development costs of this shower of new high-information products. A New Economy Much has been written about the New Economy and the consequences of the information technology revolution. A great deal of the discussion and debate has been shrouded in hype and rhetoric. But a rigorous examination of the data, and of how our economy works, shows that in fact some characteristics of our economy have changed in important ways. And while it won’t cure the ills of poverty and inequality, the New Economy will ultimately shower benefits on Americans, rich and poor. In spite of the sharp increase in inequality associated with an information age, our analysis implies that the welfare of all groups in society will increase with an information revolution precisely because of the increased speed of diffusion of new products throughout the economy. Perhaps even more striking about these findings is the implication that the effects of the information revolution will continue to be felt and influence economic well being for decades to come. Thirty years from now, Americans may consider the Internet and the personal computer to be older technologies, and will likely take them for granted. But they will still be benefiting from the forces these innovations set into motion. Thomas Cooley is the Paganelli-Bull professor of economics and Dean of NYU Stern. Mehmet Yorukoglu is an assistant professor of economics and social sciences at the University of Chicago. |