By Xavier Gabaix and Augustin Landier

It may be tempting to blame greedy CEOs and lazy boards for runaway executive pay. But a study shows top executives' salaries are rising in direct proportion to top companies' size and value. |

he rise in executive compensation in the United States in recent decades has triggered a large amount of public controversy and academic study. Critics are quick to point out that the wages of chief executive officers have skyrocketed in a period when earnings of typical workers have grown far more slowly. And in the early years of this decade, when many executives took home large compensation packages even as the stock market tanked, investors felt like salt was being rubbed in their wounds.

he rise in executive compensation in the United States in recent decades has triggered a large amount of public controversy and academic study. Critics are quick to point out that the wages of chief executive officers have skyrocketed in a period when earnings of typical workers have grown far more slowly. And in the early years of this decade, when many executives took home large compensation packages even as the stock market tanked, investors felt like salt was being rubbed in their wounds.

Scholars have generally used three types of economic arguments to explain the phenomenon of rising CEO pay. The first explanation attributes the rise to the widespread adoption of compensation packages with high-powered incentives like stock options, performance bonuses, and restricted stock since the late 1980s. And with greater volatility in the business environment, risk-averse CEOs must be offered – and paid – compensation packages that have higher value to compensate for their riskiness in order to keep them on the job.

n the post-Enron era, a second explanation gained momentum. Lucian Bebchuk of Harvard University, a proponent of the “skimming” view, argues that CEO compensation can be explained by an increase in managerial entrenchment. Secure in their positions, and operating with little effective oversight, “managers will seek to take full advantage of it and will push firms toward an equilibrium in which they can do so.” In this view, stock-option plans are seen as a way to increase CEO compensation without attracting too much notice from the shareholders. A milder form of the skimming view has been expressed by scholars who attribute the explosion in the level of stock-option pay to an inability of boards to evaluate the true costs of this form of compensation.

n the post-Enron era, a second explanation gained momentum. Lucian Bebchuk of Harvard University, a proponent of the “skimming” view, argues that CEO compensation can be explained by an increase in managerial entrenchment. Secure in their positions, and operating with little effective oversight, “managers will seek to take full advantage of it and will push firms toward an equilibrium in which they can do so.” In this view, stock-option plans are seen as a way to increase CEO compensation without attracting too much notice from the shareholders. A milder form of the skimming view has been expressed by scholars who attribute the explosion in the level of stock-option pay to an inability of boards to evaluate the true costs of this form of compensation.

“A-list movie stars have the potential to turn an average movie into a blockbuster and change the economic model for the studios – and thus command astronomical salaries – while most other actors earn far less. Just so, the market for CEOs produces a fat-tailed distribution curve, with those at the very top earning much more than those in the middle.” |

A third explanation attributes the increase to changes in the nature of the CEO job. To compensate CEOs for the increased likelihood that they will be fired, companies must pay them more in the short term. And some scholars have noted that CEO jobs have increasingly placed a greater emphasis on general rather than firm-specific skills, a trend that increases CEOs’ outside options and thus places upward pressure on pay.

A New Model

We’ve chosen to look at executive compensation through the prism of a different model, which has led us to reach quite a different conclusion. Rising CEO compensation isn’t a function of the greater use of stock options, the presence of more greedy bosses, or a fundamental shift in the nature of the position. Rather, rising CEO pay in the last 25 years has largely been a function of the substantial growth in the size and market value of US firms.

We set out to develop a simple, tractable, and calibratable competitive model of CEO pay: what might be called a neoclassical model of equilibrium CEO compensation. The model involves a lot of equations and number-crunching (the full text can be seen at Professor Landier’s website: http://pages.stern.nyu.edu/~alandier/), but it can be pared down to its essentials. CEOs have observable managerial talent and are matched to assets in a competitive assignment model. Companies pick the potential manager that maximizes performance net of salary. And the best CEOs go to the bigger firms, which maximizes their impact. The marginal impact of a CEO’s talent is assumed to increase with the value of the assets under his control. Under very general conditions, then, the compensation of a CEO is a function of the scarcity of CEOs who are judged capable of running large firms, the firm’s market value, and the market value of the other large firms.

The most basic prediction of our theory is that the average CEO compensation should be proportional to the average size of the firms in that group, and that it should grow accordingly. Now, in the US, between 1980 and 2003, the average asset market value of the largest 500 firms (including debt and equity) increased (in real terms) by a factor of six – i.e., it rose 500 percent. This rise can be decomposed as follows: both the asset price to earnings ratio and earnings have increased by a factor of approximately 2.5 during that period. The model therefore predicts that CEO pay should increase by a factor of six.

Did it? To find out, we used two different indices of CEO compensation. The first was based on the data of Michael Jensen, Kevin Murphy, and Eric Wruck, whose sample runs from 1970 onwards and is based on all CEOs included in the S&P 500, using data from Forbes and ExecuComp. Their measure of CEO total pay includes cash, restricted stock, payouts from long-term pay programs, and the value of stock options granted using ExecuComp’s modified Black-Scholes approach. (A shortcoming of these data is that total pay prior to 1978 excludes option grants, and total pay between 1978 and 1991 is computed using the amounts realized from exercising stock options, rather than grant-date values. The latter can create a mechanical positive correlation between stock-market valuations and pay in the short-run.)

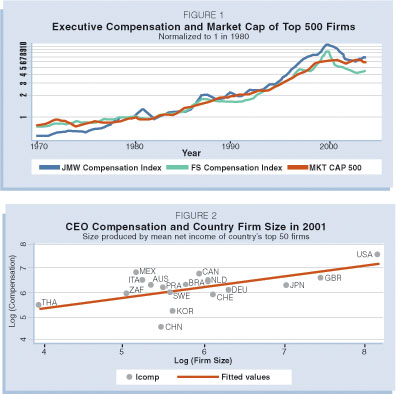

Our second index was based on the data from Carola Frydman and Raven Saks, and includes cash compensation, bonuses, and the Black-Scholes value of options on the date they were granted. The data are based on the three highest-paid officers in the largest 50 firms in the US in 1940, 1960, and 1990. The correlation of the mean asset value of the top 500 companies in Compustat is 0.93 with the first dataset and 0.97 with the second data set. When we charted the data (see Figure 1), an interesting pattern emerged: CEO compensation as produced by both datasets closely tracks the rise of market capitalization. In other words, it seems the six-fold increase of CEO pay between 1980 and 2000 can be fully attributed to the increase in market capitalization of large US companies.

Global View

It is frequently noted that in the US, CEOs are paid far more than their counterparts in Europe and Asia. And so we thought it would be useful to evaluate comparative CEO pay across countries using the model. The model predicts that CEOs heading similar firms in different countries will earn different salaries. If there are two firms of equal size, one German, one American, our model predicts the salary of the American CEO would be higher than that of the German CEO because large American companies are in substantially larger number, so that the competition of firms to hire top-managerial talent is higher. Indeed, despite a recent trend, national CEO markets are still quite segmented, e.g., due to language barriers. Our model also predicts that countries where stocks have risen at a less robust rate than stocks have in the US would also show lower executive compensation growth.

esting the model internationally is challenging. In most countries, public disclosure about executive compensation is either non-existent or much less complete than in the US. The variation in tax systems, pension benefits, perquisites, and cost of living across countries also makes comparisons difficult. We constructed international compensation figures using public information from a compensation consulting company (Towers Perrin).

The Towers Perrin survey provides levels of CEO pay across countries for a typical company with $500 million of sales in 2001. To get information on a country’s typical firms, we used Compustat global data for 2000. For each country, we computed the median net income of the top 50 firms, which gives us a proxy for the country-specific reference firm size. We chose net income as a measure of firm size, because market capitalization is absent from the Compustat Global data set. We chose 50 firms, because requiring a markedly higher number of firms would lead drop too many countries from the sample. When we ran regression analysis on these figures, we found that the variation in typical firm size accounts for about a half of the variance in CEO compensation across countries. (See Figure 2)

The Towers Perrin survey provides levels of CEO pay across countries for a typical company with $500 million of sales in 2001. To get information on a country’s typical firms, we used Compustat global data for 2000. For each country, we computed the median net income of the top 50 firms, which gives us a proxy for the country-specific reference firm size. We chose net income as a measure of firm size, because market capitalization is absent from the Compustat Global data set. We chose 50 firms, because requiring a markedly higher number of firms would lead drop too many countries from the sample. When we ran regression analysis on these figures, we found that the variation in typical firm size accounts for about a half of the variance in CEO compensation across countries. (See Figure 2)

Interestingly, country characteristics that have often been put forth as important determinants of variations in executive CEO compensation across countries, such as the percentage of family-controlled companies, or social attitudes toward inequality (which can be retrieved from the World Value Survey), have no predictive power once controlling for our measure of firm size.

Surprising Findings

The model also produced some surprising findings. Perhaps the most surprising one is that the dispersion of CEO talent distribution appeared to be extremely small at the top. If we rank CEOs by talent, and, at the head of a firm, replace CEO number one by CEO number 250, the value of that firm will decrease by only 0.02 percent. This means that the spacings between talents can look very small. However, these very small talent differences translate into considerable compensation differentials, as they are magnified by the size of very large firms. If there is a paradox in CEO pay, it is that firms must think that talent differentials between the top CEOs are small. Otherwise, they would be willing to pay CEOs much more.

few additional remarks are in order when considering executive compensation. There may be other factors at work, which we have not examined with our simple benchmark model. The rise of new sectors, such as venture capital and the money management industry, might have exerted substantial upward pressure on CEO pay in the period we studied. The dynamics of compensation in a specific industry, say the finance industry, can have large “contagion” effects to the rest of the economy. Also, it is often casually argued that a large amount of herding drives the dynamics of CEO compensation. If a few firms increase compensation (for example, because they believe talent impact has increased) the others might somehow be “forced to follow.” Here again, other firms might be forced to align their compensation policy to these new standards. Our model allows us to calibrate such contagion effects, whether they are due to market forces or not. For example, we predict that if 1 percent of the firms pay their manager twice as much as the market (e.g., due to poor corporate governance), then all firms will have to increase CEO compensation by 5 percent.

few additional remarks are in order when considering executive compensation. There may be other factors at work, which we have not examined with our simple benchmark model. The rise of new sectors, such as venture capital and the money management industry, might have exerted substantial upward pressure on CEO pay in the period we studied. The dynamics of compensation in a specific industry, say the finance industry, can have large “contagion” effects to the rest of the economy. Also, it is often casually argued that a large amount of herding drives the dynamics of CEO compensation. If a few firms increase compensation (for example, because they believe talent impact has increased) the others might somehow be “forced to follow.” Here again, other firms might be forced to align their compensation policy to these new standards. Our model allows us to calibrate such contagion effects, whether they are due to market forces or not. For example, we predict that if 1 percent of the firms pay their manager twice as much as the market (e.g., due to poor corporate governance), then all firms will have to increase CEO compensation by 5 percent.

Clearly, a superstar effect is at work here. The best managers are paired with the largest firms, which allows them to command a high compensation. A-list movie stars have the potential to turn an average movie into a blockbuster, and change the economic model for the studios – and thus command astronomical salaries – while most other actors earn far less. Just so, the market for CEOs produces a fat-tailed distribution curve, with those at the very top earning much more than those in the middle. It would be interesting to apply the analytics of the present paper to these markets such as finance, law, and entertainment and see to what extent variations in the sizes of stakes (size of funds, size of contested amounts in lawsuits, concert revenues, movie revenues) explain the evolution in top pay in these markets.

In every such instance, scholars would not be surprised to find that compensation bears a direct relation to the size of the enterprise involved, and to the competition for the talent in question. And perhaps that is the most significant contribution this model can make to the discussion about executive compensation. There is no doubt that many factors help determine the composition of executive compensation. But in the end, CEOs’ pay is determined by two interconnected and very large markets – the market for talent and skills and the market for stocks. The money at stake for the stockholders, which has massively increased in the last decades, is the main determinant of CEO compensation levels.

Xavier Gabaix is associate professor of economics at the Massachusetts Institute of Technology. Augustin Landier is assistant professor of finance at NYU Stern.